bootridge

Empirical Bayes penalized regression for univariate or multivariate outcomes,

with shrinkage tuned to minimize prediction error computed by .632 bootstrap.

-- Function File: bootridge (Y, X)

-- Function File: bootridge (Y, X, CATEGOR)

-- Function File: bootridge (Y, X, CATEGOR, NBOOT)

-- Function File: bootridge (Y, X, CATEGOR, NBOOT, ALPHA)

-- Function File: bootridge (Y, X, CATEGOR, NBOOT, ALPHA, L)

-- Function File: bootridge (Y, X, CATEGOR, NBOOT, ALPHA, L, DEFF)

-- Function File: bootridge (Y, X, CATEGOR, NBOOT, ALPHA, L, DEFF, SEED)

-- Function File: bootridge (Y, X, CATEGOR, NBOOT, ALPHA, L, DEFF, SEED, TOL)

-- Function File: S = bootridge (Y, X, ...)

-- Function File: [S, YHAT] = bootridge (Y, X, ...)

'bootridge (Y, X)' fits an empirical Bayes ridge regression model using

a linear Normal (Gaussian) likelihood with an empirical Bayes normal

ridge prior on the regression coefficients. The ridge tuning constant

(lambda) is optimized via .632 bootstrap-based machine learning (ML) to

minimize out-of-bag prediction error [1, 2]. Y is an m-by-q matrix of

outcomes and X is an m-by-n design matrix whose first column must

correspond to an intercept term. If an intercept term (a column of ones)

is not found in the first column of X, one is added automatically. If any

rows of X or Y contain missing values (NaN) or infinite values (+/- Inf),

the corresponding observations are omitted before fitting.

For each outcome, the function prints posterior summaries for regression

coefficients or linear estimates, including posterior means, equal-tailed

credible intervals, Bayes factors (lnBF10), and the marginal prior used

for inference. When multiple outcomes are fitted (q > 1), the function

additionally prints posterior summaries for the residual correlations

between outcomes, reported as unique (lower-triangular) outcome pairs.

For each correlation, the printed output includes the estimated

correlation and its credible interval.

Interpretation note (empirical Bayes):

Bayes factors reported by 'bootridge' are empirical‑Bayes approximations

based on a data‑tuned ridge prior. They are best viewed as model‑

comparison diagnostics (evidence on a predictive, information‑theoretic

scale) rather than literal posterior odds under a fully specified prior

[3–5]. The log scale (lnBF10) is numerically stable and recommended

for interpretation; BF10 may be shown as 0 or Inf when beyond machine

range, while lnBF10 remains finite. These Bayesian statistics converge

to standard conjugate Bayesian evidence as the effective residual

degrees of freedom (df_t) increase.

For convenience, the statistics-resampling package also provides the

function `bootlm`, which offers a user-friendly but feature-rich interface

for fitting univariate linear models with continuous and categorical

predictors. The design matrix X and hypothesis matrix L returned in the

MAT-file produced by `bootlm` can be supplied directly to `bootridge`.

The outputs of `bootlm` also provide a consistent definition of the model

coefficients, thereby facilitating interpretation of parameter estimates,

contrasts, and posterior summaries. The design matrix X and hypothesis

matrix L can also be obtained the same way with one of the outcomes of a

multivariate data set, then fit to all the outcomes using bootridge.

'bootridge (Y, X, CATEGOR)' specifies the predictor columns that

correspond to categorical variables. CATEGOR must be a scalar or vector

of integer column indices referring to columns of X (excluding the

intercept). Alternatively, if all predictor terms are categorical, set

CATEGOR to 'all' or '*'. CATEGOR does NOT create or modify dummy or

contrast coding; users are responsible for supplying an appropriately

coded design matrix X. The indices in CATEGOR are used to identify

predictors that represent categorical variables, even when X is already

coded, so that variance-based penalty scaling is not applied to these

terms.

For categorical predictors in ridge regression, use meaningful centered

and preferably orthogonal (e.g. Helmert or polynomial) contrasts whenever

possible, since shrinkage occurs column-wise in the coefficient basis.

Orthogonality leads to more stable shrinkage and tuning of the ridge

parameter. Although the prior is not rotationally invariant, Bayes

factors for linear contrasts defined via a hypothesis matrix (L) are

typically more stable when the contrasts defining the coefficients are

orthogonal.

'bootridge (Y, X, CATEGOR, NBOOT)' sets the number of bootstrap samples

used to estimate the .632 bootstrap prediction error. The bootstrap* has

first order balance to improve the efficiency for variance estimation,

and utilizes bootknife (leave-one-out) resampling to guarantee

observations in the out-of-bag samples. The default value of NBOOT is

100, but more resamples are recommended to reduce monte carlo error.

The bootstrap tuning of the ridge parameter relies on resampling

functionality provided by the statistics-resampling package. In

particular, `bootridge` depends on the functions `bootstrp` and `boot` to

perform balanced bootstrap and bootknife (leave-one-out) resampling and

generate out-of-bag samples. These functions are required for estimation

of the .632 bootstrap prediction error used to select the ridge tuning

constant.

'bootridge (Y, X, CATEGOR, NBOOT, ALPHA)' sets the central mass of equal-

tailed credibility intervals (CI) to (1 - ALPHA) with probability mass

ALPHA/2 in each tail, and sets the threshold for the adjusted stability

selection (SS) probabilities of the regression coefficients to (1 - ALPHA).

ALPHA must be a scalar value between 0 and 1. The default value of ALPHA

is 0.05 for 95% intervals.

'bootridge (Y, X, CATEGOR, NBOOT, ALPHA, L)' specifies a hypothesis

matrix L of size n-by-c defining c linear contrasts or model-based

estimates of the regression coefficients. In this case, posterior

summaries and credible intervals are reported for the linear estimates

rather than the model coefficients.

'bootridge (Y, X, CATEGOR, NBOOT, ALPHA, L, DEFF)' specifies a design

effect used to account for clustering or dependence. DEFF inflates the

posterior covariance and reduces the effective degrees of freedom (df_t)

to ensure Bayes factors and intervals are calibrated for the effective

sample size. For a mean, Kish's formula DEFF = 1+(g-1)*r (where g is

cluster size) suggests an upper bound of g. However, for regression

slopes, the realized DEFF depends on the predictor type: it can exceed

g for between-cluster predictors or be less than 1 for within-cluster

predictors. DEFF is best estimated as the ratio of clustered-to-i.i.d.

sampling variances - please see DETAIL below. Default DEFF is 1.

'bootridge (Y, X, CATEGOR, NBOOT, ALPHA, L, DEFF, SEED)' initialises the

Mersenne Twister random number generator using an integer SEED value so

that bootstrap results are reproducible, which improves convergence.

Monte carlo error of the results can be assessed by repeating the

analysis multiple times, each time with a different random seed.

'bootridge (Y, X, CATEGOR, NBOOT, ALPHA, L, DEFF, SEED, TOL)' controls

the convergence tolerance for optimizing the ridge tuning constant lambda

on the log10 scale. Hyperparameter optimization terminates when the width

of the current bracket satisfies:

log10 (lambda_high) − log10 (lambda_low) < TOL.

Thus, TOL determines the relative (multiplicative) precision of lambda.

The default value TOL = 0.005 corresponds to approximately a 1% change in

lambda, which is typically well below the Monte Carlo noise of the .632

bootstrap estimate of prediction error.

* If sufficient parallel resources are available (three or more workers),

the optimization uses a parallel k‑section search; otherwise, a serial

golden‑section search is used. The tolerance TOL applies identically

in both cases. The benefit of parallel processing is most evident when

NBOOT is very large. In GNU Octave, the maximum number of workers used

can be set by the user before running bootridge, for example, for three

workers with the command:

setenv ('OMP_NUM_THREADS', '3')

'S = bootridge (Y, X, ...)' returns a structure containing posterior

summaries including posterior means, credibility intervals, Bayes factors,

prior summaries, the bootstrap-optimized ridge parameter, residual

covariance estimates, and additional diagnostic information.

The output S is a structure containing the following fields (listed in

order of appearance):

o coefficient

n-by-q matrix of posterior mean regression coefficients for each

outcome when no hypothesis matrix L is specified.

o estimate

c-by-q matrix of posterior mean linear estimates when a hypothesis

matrix L is specified. This field is returned instead of

'coefficient' when L is non-empty.

o CI_lower

Matrix of lower bounds of the (1 - ALPHA) credibility intervals

for coefficients or linear estimates. Dimensions match those of

'coefficient' or 'estimate'.

o CI_upper

Matrix of upper bounds of the (1 - ALPHA) credibility intervals

for coefficients or linear estimates. Dimensions match those of

'coefficient' or 'estimate'.

o BF10

Matrix of Bayes factors (BF10) for testing whether each regression

coefficient or linear estimate equals zero, computed using the

Savage–Dickey density ratio. Values may be reported as 0 or Inf

when outside floating‑point range; lnBF10 remains finite and is

the recommended evidential scale.

o lnBF10

Matrix of natural logarithms of the Bayes factors (BF10). Positive

values indicate evidence in favour of the alternative hypothesis,

whereas negative values indicate evidence in favour of the null.

lnBF10 < -1 is approx. BF10 < 0.3

lnBF10 > +1 is approx. BF10 > 3.0

o prior

Cell array describing the marginal inference-scale prior used for

each coefficient or estimate in Bayes factor computation.

Reported as 't (mu, sigma, df_t)' on the coefficient (or estimate)

scale; see CONDITIONAL VS MARGINAL PRIORS for details.

o Deff

Design effect used to inflate the residual covariance and reduce

inferential degrees of freedom to account for clustering.

o lambda

Scalar ridge tuning constant selected by minimizing the .632

bootstrap estimate of prediction error (then scaled by DEFF).

o df_lambda

Effective residual degrees of freedom under ridge regression,

defined as m minus the trace of the ridge hat matrix. Used for

residual variance estimation (scale); does NOT include DEFF.

o df_t

Inferential degrees of freedom, which is df_lambda adjusted for

for the design effect.

o Sigma_Y_hat

Estimated residual covariance matrix of the outcomes, inflated by

the design effect DEFF when applicable. For a univariate outcome,

this reduces to the residual variance.

o tau2_hat

Estimated prior covariance of the regression coefficients across

outcomes, proportional to Sigma_Y_hat and inversely proportional

to the ridge parameter lambda.

o Sigma_Beta

Cell array of posterior covariance matrices of the regression

coefficients. Each cell corresponds to one outcome and contains

the covariance matrix for that outcome.

o nboot

Number of bootstrap samples used to estimate the .632 bootstrap

prediction error.

o tol

Numeric tolerance used in the golden-section search for optimizing

the ridge tuning constant.

o iter

Number of iterations performed by the golden-section search.

o pred_err

The minimized prediction error calculated using the optimal lambda.

Note that pred_err calculation is summed over outcome variables

(columns) from the fit on Y (after internal standardization), using

the predictors X (after internal centering).

o RSQ_pred

The predicted R-squared for the fit across all the outcomes.

RSQ_pred (average) = 1 - (S.pred_err / q),

where q is the number of outcomes.

o stability

The probabilities that the sign of the regression coefficients

remained consistent across max(nboot,1999) bootstrap resamples [6].

Raw probabilities are smoothed using a Jeffreys prior and, if

applicable, adjusted by the design effect (Deff). In the printed

summary, stability exceeding (1 - ALPHA / 2) is indicated by (+)

or (-) to denote the consistent direction of the effect.

o RTAB

Matrix summarizing residual correlations (strictly lower-

triangular pairs). The columns correspond to outcome J, outcome I,

and the coefficient and credible intervals for their correlation.

Credible intervals for correlations are computed on Fisher’s z

[7] using a t‑based sampling distribution with effective degrees

of freedom df_t, and then back‑transformed. See CONDITIONAL VS

MARGINAL PRIORS and DETAIL below. Diagonal entries are undefined

and not included.

o P_vec

A vector of predictor-wise penalty weights used to normalize

shrinkage across the predictor terms.

'[S, YHAT] = bootridge (Y, X, ...)' returns fitted values.

DETAIL: The model implements an empirical Bayes ridge regression that

simultaneously addresses the problems of multicollinearity, multiple

comparisons, and clustered dependence. The sections below provide

detail on the applications to which this model is well suited and the

principles of its operation.

REGULARIZATION AND MULTIPLE COMPARISONS:

Unlike classical frequentist methods (e.g., Bonferroni) that penalize

inference-stage decisions (p-values), `bootridge` penalizes the estimates

themselves via shrinkage. By pooling information across all predictors to

learn the global penalty (lambda), the model automatically adjusts its

skepticism to the design's complexity. This provides a principled

probabilistic alternative to family-wise error correction: noise-driven

effects are shrunken toward zero, while stable effects survive the

penalty. This "Partial Pooling" ensures that Bayes factors are

appropriately conservative without the catastrophic loss of power

associated with classical post-hoc adjustments [8, 9]. See later section

on STATISTICAL INFERENCE AND ERROR CONTROL.

PREDICTIVE OPTIMIZATION:

The ridge tuning constant (hyperparameter) is selected empirically by

minimizing the .632 bootstrap estimate of prediction error [1, 2]. This

aligns lambda with minimum estimated out‑of‑sample mean squared

prediction error, ensuring the model is optimized for generalizability

rather than mere in-sample fit [10–12]. This lambda in turn determines the

scale of the Normal ridge prior used to shrink slope coefficients toward

zero [13].

CONDITIONAL VS MARGINAL PRIORS:

The ridge penalty (lambda) corresponds to a Normal prior on the

regression coefficients CONDITIONAL on the residual variance:

Beta | sigma^2 ~ Normal(0, tau^2 * sigma^2),

where tau^2 is determined by lambda. This conditional Normal prior

fully defines the ridge objective function and is held fixed during

lambda optimisation (prediction-error minimisation).

For inference, however, uncertainty in the residual variance is

explicitly acknowledged. Integrating over variance uncertainty under

an empirical‑Bayes approximation induces a marginal Student’s t

distribution for coefficients and linear estimates, which is used

for credible intervals and Bayes factors.

PRIOR CALIBRATION & DATA INDEPENDENCE:

To prevent circularity in the prior selection, lambda is optimized

solely by minimizing the .632 bootstrap out-of-bag (OOB) error.

This ensures the prior precision is determined by the model's

ability to predict "unseen" observations (data points not used

for the coefficient estimation in a given bootstrap draw),

thereby maintaining a principled separation between the data used

for likelihood estimation and the data used for prior tuning.

STABILITY SELECTION:

The directional reproducibility of the sign of the regression coefficients

under resampling are quantified and reported as Stability Selection (SS).

It is possible for a shrunken coefficient to be highly stable in sign

despite having anecdotal Bayes Factors.

BAYES FACTORS:

For regression coefficients and linear estimates, Bayes factors are

computed using the Savage–Dickey density ratio evaluated on the

marginal inference scale. Prior and posterior densities are Student’s

t distributions with shared degrees of freedom (df_t), reflecting

uncertainty in the residual variance under an empirical‑Bayes

approximation [3–5].

For residual correlations between outcomes, credible intervals are

computed on Fisher’s z [7] with effective degrees of freedom df_t and

then back‑transformed to r.

SUMMARY OF PRIORS:

The model employs the following priors for empirical Bayes inference:

o Intercept: Improper flat/Uniform prior, U(-Inf, Inf).

o Slopes: Marginal Student’s t prior on the coefficient (or estimate)

scale, t(0, sigma_prior, df_t), with scale determined by the

bootstrap‑optimised ridge parameter (lambda) and design effect

DEFF.

In the limit (high df_t), the inferential framework converges to a

Normal-Normal conjugate prior where the prior precision is

determined by the optimized lambda. At lower df_t, the function

provides more robust, t-marginalized inference to account for

uncertainty in the error variance.

o Residual Variance: Implicit (working) Inverse-Gamma prior,

Inv-Gamma(df_t/2, Sigma_Y_hat), induced by variance estimation

and marginalization and used to generate the t-layer.

o Correlations: An improper flat prior is assumed on Fisher’s z

transform of the correlation coefficients. Under this prior, the

posterior for z is proportional to the t‑based sampling distribution

implied by the effective degrees of freedom df_t.

UNCERTAINTY AND CLUSTERING:

The design effect specified by DEFF is integrated throughout the model

consistent with its definition:

DEFF(parameter) = Var_true(parameter) / Var_iid(parameter)

This guards against dependence between observations leading to anti-

conservative inference. This adjustment occurs at three levels:

1. Prior Learning: The ridge tuning constant (lambda) is selected by

minimizing predictive error on the i.i.d. bootstrap scale and then

divided by DEFF. This "dilutes" the prior precision, ensuring the

lambda_iid = sigma^2 / tau^2_iid

tau^2_true = DEFF * tau^2_iid

lambda_true = sigma^2 / tau^2_true = lambda_iid / DEFF

where sigma^2 (a.k.a. Sigma_Y_hat) is residual variance (data space)

and tau^2 (a.k.a. tau2_hat) is the prior variance (parameter space).

2. Scale Estimation: Residual variance (Sigma_Y_hat) is estimated using

the ridge-adjusted degrees of freedom (df_lambda = m - trace(H_lambda))

and is then inflated by a factor of DEFF. This yields an "effective"

noise scale on the derived parameter statistics that accounts for

within-cluster correlation [14, 15] according to:

Var_true(beta_hat) = DEFF * Var_iid(beta_hat)

3. Inferential Shape: A marginal Student’s t layer is used for all

quantiles and Bayes factors to propagate uncertainty in the

residual variance and effective sample size. To prevent over-

certainty in small-cluster settings, the inferential degrees of

freedom are reduced:

df_t = (m / DEFF) - trace (H_lambda), where m is size (Y, 1)

This ensures that both the scale (width) and the shape (tails) of the

posterior distributions are calibrated for the effective sample size.

The use of t‑based adjustments is akin to placing an Inverse-Gamma

prior (alpha = df_t / 2, beta = Sigma_Y_hat) on the residual variance

and is in line with classical variance component approximations (e.g.,

Satterthwaite/Kenward–Roger) and ridge inference recommendations

[16–18].

4. Stability Selection: The sign-consistency probabilities (denoted as

stability) under bootstrap resampling are adjusted for the design

effect via a Probit-link transformation:

Phi ( Phi^-1(stability) / sqrt (Deff) )

Where Phi and Phi^-1 are the cumulative standard normal distribution

function and its inverse respectively. This adjustment ensures that

the reported stability reflects the effective sample size rather than

the raw number of observations, preventing over-certainty in the

presence of clustered or dependent data.

ESTIMATING THE DESIGN EFFECT:

While DEFF = 1 + (g - 1) * r provides a useful analytical upper bound

based on cluster size (g) and intraclass correlation (r), the realized

impact of dependence on regression slopes often varies by predictor type.

For complex designs, DEFF is best estimated as the mean ratio of the

parameter variances—obtained from the variances of the bootstrap

distributions under a cluster-robust estimator (e.g., wild cluster

bootstrap via `bootwild` or cluster-based bayesian bootstrap via

`bootbayes`) relative to an i.i.d. assumption. Supplying this

"Effective DEFF" allows `bootridge` to provide analytical Bayesian

inference that approximates the results of a full hierarchical or

resampled model [14, 15].

DIAGNOSTIC ASSESSMENT:

Users should utilize `bootlm` for formal diagnostic plots (Normal

Q-Q, Spread-Location, Cook’s Distance). These tools identify

influential observations that may require inspection before or

after ridge fitting.

SUITABILITY:

This function is designed for models with continuous outcomes and

assumes a linear Normal (Gaussian) likelihood. It is not suitable for

binary, count, or categorical outcomes. However, binary and categorical

predictors are supported.

INTERNAL SCALING AND STANDARDIZATION:

All scaling and regularization procedures for optimizing the ridge

parameter are handled internally to ensure numerical stability and

balanced, scale-invariant shrinkage. To ensure all outcomes contribute

equally to the global regularization regardless of their units, the

ridge parameter (lambda) is optimized using internally standardized

outcomes.

When refitting the model with the optimal ridge parameter, while

predictors are maintained on their original scale, the ridge penalty

matrix is automatically constructed with diagonal elements proportional

to the column variances of X. This ensures that the shrinkage applied

to coefficients is equivalent to that of standardized predictors,

without requiring manual preprocessing (categorical terms are identified

via CATEGOR and are exempt from this variance-based penalty scaling).

Following optimization, the final model is refit to the outcomes on

their original scale; consequently, all posterior summaries,

credibility intervals, and prior standard deviations are reported

directly on the original coefficient scale for ease of interpretation.

STATISTICAL INFERENCE AND ERROR CONTROL:

Inference is provided via three complementary metrics: Credibility

Intervals (CI), Bayes Factors (BF), and Stability Selection (SS)

probabilities. Conditioned on a bootstrap-optimized ridge penalty, these

statistics exhibit superior control over Type M (magnitude) and Type S

(sign) errors relative to unpenalized estimators. The inherent shrinkage

provides implicit False Discovery Rate (FDR) control for CIs and BFs by

suppressing noise-driven inflation, providing more conservative global

error control than unpenalized methods. Conversely, SS probabilities

prioritize statistical power in sparse or low signal-to-noise ratio (SNR)

settings; while SS maintains marginal False Positive Rate (FPR) control

near ALPHA, it lacks the intrinsic FDR protection afforded by shrinkage

when interpreting multiple simultaneous inferences. The reliability of

all metrics improves as the Signal-to-Noise Ratio (SNR) increases.

CI BF SS

FDR-Controlled <----------------------------> FPR-Controlled

(High Stringency) (High Discovery)

See the last demo in this function for simulation code and results

supporting these claims.

See also: `bootstrp`, `boot`, `bootlm`, `bootbayes` and `bootwild`.

Bibliography:

[1] Delaney, N. J. & Chatterjee, S. (1986) Use of the Bootstrap and Cross-

Validation in Ridge Regression. Journal of Business & Economic Statistics,

4(2):255–262. https://doi.org/10.1080/07350015.1986.10509520

[2] Efron, B. & Tibshirani, R. J. (1993) An Introduction to the Bootstrap.

New York, NY: Chapman & Hall, pp. 247–252.

https://doi.org/10.1201/9780429246593

[3] Dickey, J. M. & Lientz, B. P. (1970) The Weighted Likelihood Ratio,

Sharp Hypotheses about Chances, the Order of a Markov Chain. Ann. Math.

Statist., 41(1):214–226. (Savage–Dickey)

https://doi.org/10.1214/aoms/1177697203

[4] Morris, C. N. (1983) Parametric Empirical Bayes Inference: Theory and

Applications. JASA, 78(381):47–55. https://doi.org/10.2307/2287098

[5] Wagenmakers, E.-J., Lodewyckx, T., Kuriyal, H., & Grasman, R. (2010)

Bayesian hypothesis testing for psychologists: A tutorial on the

Savage–Dickey method. Cognitive Psychology, 60(3):158–189.

https://doi.org/10.1016/j.cogpsych.2009.12.001

[6] Meinshausen, N. & Buhlmann, P. (2010) Stability selection. J. R. Statist.

Soc. B. 72(4): 417-473. https://doi.org/10.1111/j.1467-9868.2010.00740.x

[7] Fisher, R. A. (1921) On the "Probable Error" of a Coefficient of

Correlation Deduced from a Small Sample. Metron, 1:3–32. (Fisher z)

[8] Gelman, A., Hill, J., & Yajima, M. (2012) Why we usually don't worry

about multiple comparisons. J. Res. on Educ. Effectiveness, 5:189–211.

https://doi.org/10.1080/19345747.2011.618213

[9] Efron, B. (2010) Large-Scale Inference: Empirical Bayes Methods for

Estimation, Testing, and Prediction. Cambridge University Press.

https://doi.org/10.1017/CBO9780511761362

[10] Hastie, T., Tibshirani, R., & Friedman, J. (2009) The Elements of

Statistical Learning (2nd ed.). Springer.

https://doi.org/10.1007/978-0-387-84858-7

[11] Ye, J. (1998) On Measuring and Correcting the Effects of Data Mining and

Model Selection. JASA, 93(441):120–131. (Generalized df)

https://doi.org/10.1080/01621459.1998.10474094

[12] Akaike, H. (1973) Information Theory and an Extension of the Maximum

Likelihood Principle. In: 2nd Int. Symp. on Information Theory. (AIC/KL)

https://doi.org/10.1007/978-1-4612-0919-5_38

[13] Hoerl, A. E. & Kennard, R. W. (1970) Ridge Regression: Biased Estimation

for Nonorthogonal Problems. Technometrics, 12(1):55–67.

https://doi.org/10.1080/00401706.1970.10488634

[14] Neuhaus, J. M., & Segal, M. R. (1993). Design effects for binary

regression models fitted to dependent data. Statistics in Medicine,

12(13):1259–1268. https://doi.org/10.1002/sim.4780121309

[15] Cameron, A. C., & Miller, D. L. (2015) A Practitioner's Guide to

Cluster-Robust Inference. J. Hum. Resour., 50(2):317–372.

https://doi.org/10.3368/jhr.50.2.317

[16] Satterthwaite, F. E. (1946) An Approximate Distribution of Estimates of

Variance Components. Biometrics Bulletin, 2(6):110–114.

https://doi.org/10.2307/3002019

[17] Kenward, M. G. & Roger, J. H. (1997) Small Sample Inference for Fixed

Effects from Restricted Maximum Likelihood. Biometrics, 53(3):983–997.

https://doi.org/10.2307/2533558

[18] Vinod, H. D. (1987) Confidence Intervals for Ridge Regression Parameters.

In Time Series and Econometric Modelling, pp. 279–300.

https://doi.org/10.1007/978-94-009-4790-0_19

bootridge (version 2026.02.18)

Author: Andrew Charles Penn

Demonstration 1

The following code

% Analysis of Rohwer's dataset

% Data from an experiment by William D. Rohwer on kindergarten children

% designed to examine how well performance on a set of paired-associate (PA)

% tasks can predict performance on some measures of aptitude and achievement.

% Load the dataset

fid = fopen ('rohwer_data.csv', 'r', 'l');

dat = textscan ...

(fid, '%f %s %f %f %f %f %f %f %f %f', ...

'Delimiter', ',', 'HeaderLines', 1);

[group, SES, SAT, PPVT, Raven, n, s, ns, na, ss] = dat{:};

% Define model terms - all main effects and two-way interactions with SES

mdl = [1 0 0 0 0 0; ...

0 1 0 0 0 0; ...

0 0 1 0 0 0; ...

0 0 0 1 0 0; ...

0 0 0 0 1 0; ...

0 0 0 0 0 1; ...

1 1 0 0 0 0; ...

1 0 1 0 0 0; ...

1 0 0 1 0 0; ...

1 0 0 0 1 0; ...

1 0 0 0 0 1];

% Fit linear model with one of the outcomes to obtain design matrix

MAT = bootlm (SAT, {SES, n, s, ns, na, ss}, 'model', 'linear', ...

'nboot', 0, 'display', 'off', 'continuous', [2:6], ...

'contrasts', 'simple', 'model', mdl);

% Run machine learning optimized ridge regression with empirical bayes

% inference. By not assigning the output to a variable, we get results

% printed to stdout.

fprintf ('The bootridge function is running ...\n')

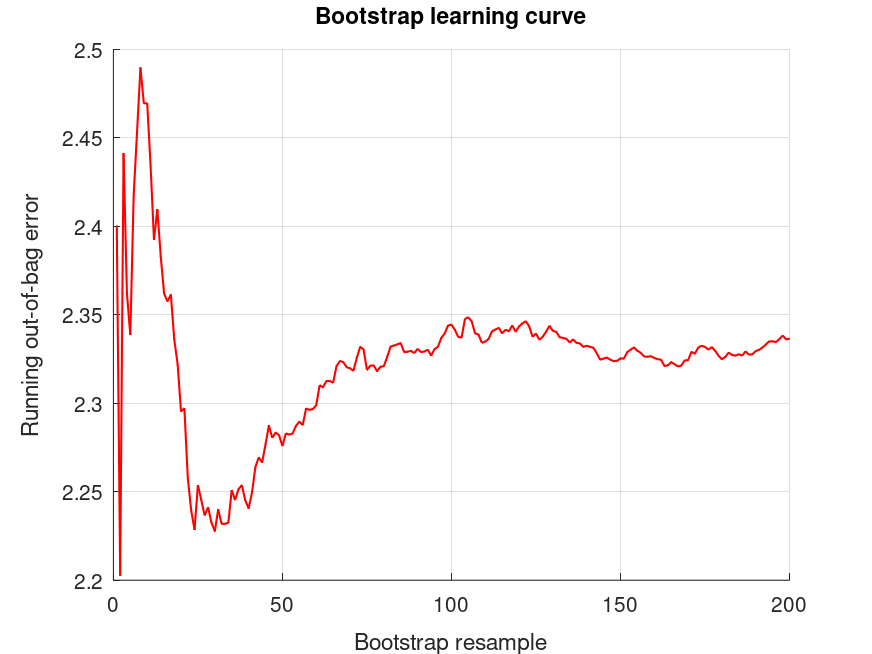

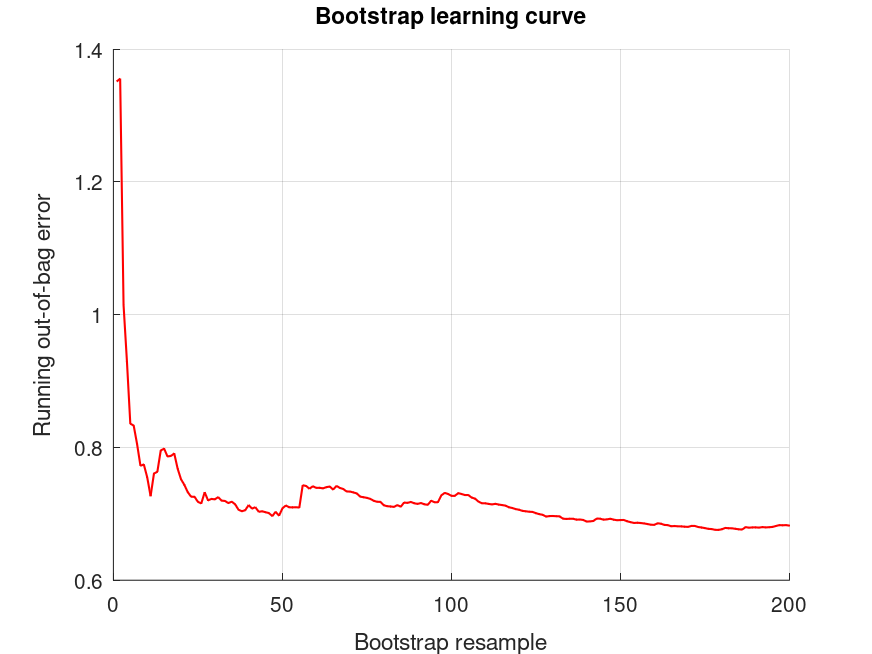

bootridge ([SAT, PPVT, Raven], MAT.X, 2, 200, .05);

% Get the output structure stored in ans from the last function call

S = ans;

Produces the following output

The bootridge function is running ... Empirical Bayes Ridge Regression (.632 Bootstrap Tuning) - Summary ******************************************************************************* Number of predictors (p): 11 Number of outcomes (q): 3 Sample size: 69 Design effect (Deff): 1 Bootstrap resamples (nboot): 200 Minimized .632 bootstrap prediction error: 2.07996 Predicted R-squared: 0.307 (30.7%) Bootstrap optimized ridge tuning constant (lambda): 7.25059 Effective residual degrees of freedom (df_lambda): 59.3 Residual variances (range): [7.68, 564] Inferential degrees of freedom (df_t): 59.3 Used for credible intervals and Bayes factors below. 95% credible intervals for correlations between outcomes: (Prior on Fisher's z is flat/improper) Outcome J Outcome I correlation CI_lower CI_upper 1 2 +0.2149 -0.04599 +0.4484 1 3 +0.2957 +0.04040 +0.5147 2 3 +0.2968 +0.04166 +0.5156 95% credible intervals and Bayes factors for regression coefficients. Global ridge prior contribution to posterior precision: 20.77 % Stability selection (SS): >97.5% for the (-) or (+) sign of the coefficient. SS probabilities are reported in S.stability Outcome 1: coefficient CI_lower CI_upper lnBF10 SS prior +37.87 +31.77 +43.98 +NaN U (-Inf, Inf) +6.490 -3.554 +16.53 +0.275 t (0, 8.82, 59.3) +1.185 -0.7453 +3.115 -0.129 t (0, 2.34, 59.3) +1.113 -0.4437 +2.670 +0.0729 t (0, 2.01, 59.3) -2.441 -3.920 -0.9626 +4.31 (-) t (0, 1.61, 59.3) +2.127 +0.7229 +3.531 +3.64 (+) t (0, 1.42, 59.3) +0.8202 -0.5386 +2.179 -0.0338 t (0, 1.46, 59.3) +2.592 -1.316 +6.500 -0.0302 t (0, 4.87, 59.3) +2.241 -0.8743 +5.356 +0.0852 t (0, 4.03, 59.3) -2.339 -5.306 +0.6272 +0.460 t (0, 3.23, 59.3) +3.362 +0.5435 +6.179 +2.05 (+) t (0, 2.87, 59.3) -1.699 -4.450 +1.053 -0.0223 t (0, 3.02, 59.3) Outcome 2: coefficient CI_lower CI_upper lnBF10 SS prior +72.38 +69.54 +75.21 +NaN U (-Inf, Inf) +11.51 +6.840 +16.17 +9.81 (+) t (0, 4.10, 59.3) +0.2438 -0.6527 +1.140 -0.736 t (0, 1.09, 59.3) -0.1094 -0.8324 +0.6136 -0.903 t (0, 0.934, 59.3) -0.1821 -0.8689 +0.5047 -0.636 t (0, 0.748, 59.3) +1.126 +0.4736 +1.778 +4.82 (+) t (0, 0.658, 59.3) +0.5167 -0.1144 +1.148 +0.568 t (0, 0.679, 59.3) -0.1079 -1.923 +1.707 -0.905 t (0, 2.26, 59.3) +0.7991 -0.6477 +2.246 -0.335 t (0, 1.87, 59.3) +0.006221 -1.372 +1.384 -0.780 t (0, 1.50, 59.3) +0.09108 -1.218 +1.400 -0.701 t (0, 1.33, 59.3) +0.1488 -1.129 +1.427 -0.761 t (0, 1.40, 59.3) Outcome 3: coefficient CI_lower CI_upper lnBF10 SS prior +14.20 +13.48 +14.91 +NaN U (-Inf, Inf) +1.049 -0.1227 +2.221 +1.03 (+) t (0, 1.03, 59.3) +0.1118 -0.1134 +0.3371 -0.389 t (0, 0.273, 59.3) +0.2157 +0.03400 +0.3973 +1.79 (+) t (0, 0.235, 59.3) +0.03120 -0.1414 +0.2038 -0.712 t (0, 0.188, 59.3) +0.02972 -0.1341 +0.1935 -0.636 t (0, 0.165, 59.3) -0.03604 -0.1946 +0.1225 -0.662 t (0, 0.171, 59.3) -0.1310 -0.5871 +0.3251 -0.745 t (0, 0.568, 59.3) +0.3330 -0.03056 +0.6965 +0.711 (+) t (0, 0.470, 59.3) -0.2740 -0.6202 +0.07219 +0.469 t (0, 0.377, 59.3) +0.09246 -0.2364 +0.4213 -0.551 t (0, 0.335, 59.3) -0.04850 -0.3696 +0.2726 -0.742 t (0, 0.353, 59.3)

and the following figure

| Figure 1 |

|---|

|

Demonstration 2

The following code

% Simple linear regression. The data represents salaries of employees and

% their years of experience, modified from Allena Venkata. The salaries are

% in units of 1000 dollars per annum.

years = [1.20 1.40 1.60 2.10 2.30 3.00 3.10 3.30 3.30 3.80 4.00 4.10 ...

4.10 4.20 4.60 5.00 5.20 5.40 6.00 6.10 6.90 7.20 8.00 8.30 ...

8.80 9.10 9.60 9.70 10.40 10.60]';

salary = [39 46 38 44 40 57 60 54 64 57 63 56 57 57 61 68 66 83 81 94 92 ...

98 101 114 109 106 117 113 122 122]';

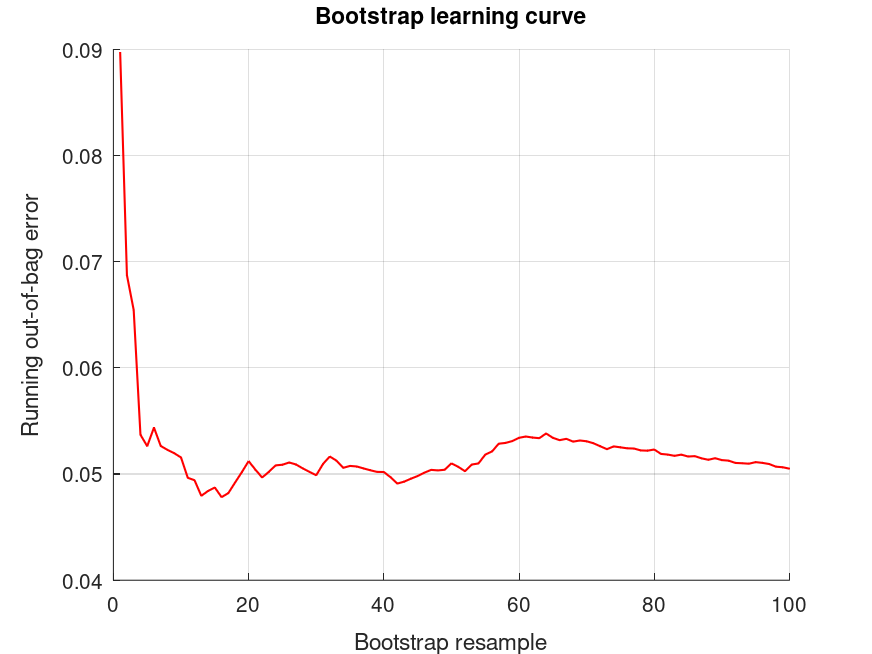

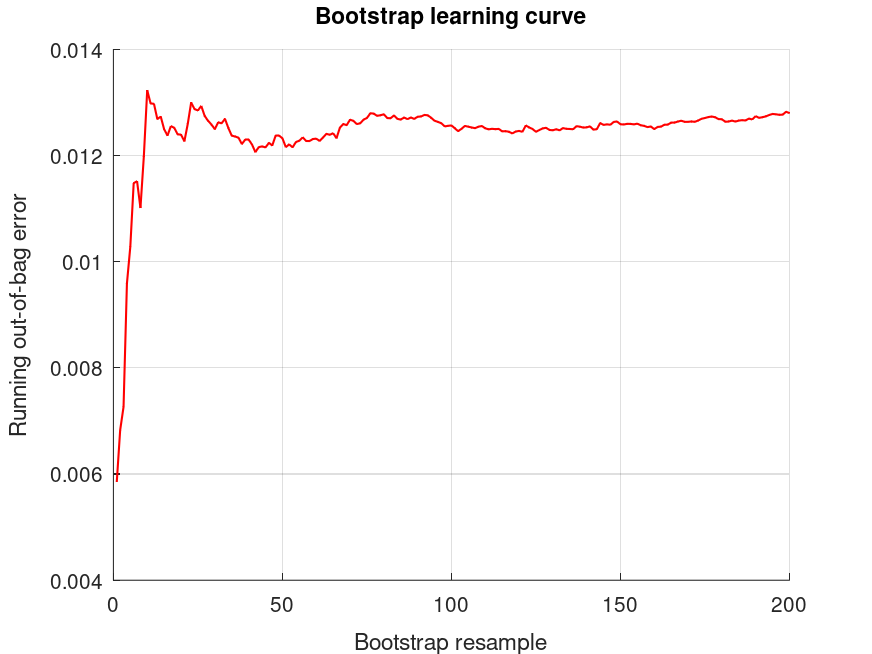

fprintf ('The bootridge function is running ...\n')

bootridge (salary, years);

% We can see from the intercept that the starting starting salary is $25.2 K

% and that salary increase per year of experience is $9.4 K.

Produces the following output

The bootridge function is running ... Empirical Bayes Ridge Regression (.632 Bootstrap Tuning) - Summary ******************************************************************************* Number of predictors (p): 1 Number of outcomes (q): 1 Sample size: 30 Design effect (Deff): 1 Bootstrap resamples (nboot): 100 Minimized .632 bootstrap prediction error: 0.045731 Predicted R-squared: 0.954 (95.4%) Bootstrap optimized ridge tuning constant (lambda): 0.0767424 Effective residual degrees of freedom (df_lambda): 28.0 Residual variance (sigma^2): 32.8 Inferential degrees of freedom (df_t): 28.0 Used for credible intervals and Bayes factors below. 95% credible intervals and Bayes factors for regression coefficients. Global ridge prior contribution to posterior precision: 0.26 % Stability selection (SS): >97.5% for the (-) or (+) sign of the coefficient. SS probabilities are reported in S.stability Outcome 1: coefficient CI_lower CI_upper lnBF10 SS prior +24.92 +20.25 +29.59 +NaN U (-Inf, Inf) +9.430 +8.663 +10.20 +42.9 (+) t (0, 7.29, 28.0)

and the following figure

| Figure 1 |

|---|

|

Demonstration 3

The following code

% One-way repeated measures design.

% The data is from a study on the number of words recalled by 10 subjects

% for three time condtions, in Loftus & Masson (1994) Psychon Bull Rev.

% 1(4):476-490, Table 2.

words = [10 13 13; 6 8 8; 11 14 14; 22 23 25; 16 18 20; ...

15 17 17; 1 1 4; 12 15 17; 9 12 12; 8 9 12];

seconds = [1 2 5; 1 2 5; 1 2 5; 1 2 5; 1 2 5; ...

1 2 5; 1 2 5; 1 2 5; 1 2 5; 1 2 5;];

subject = [ 1 1 1; 2 2 2; 3 3 3; 4 4 4; 5 5 5; ...

6 6 6; 7 7 7; 8 8 8; 9 9 9; 10 10 10];

% Frequentist framework: wild bootstrap of linear model, with orthogonal

% polynomial contrast coding followed up with treatment vs control

% hypothesis testing.

MAT = bootlm (words, {subject,seconds}, 'display', 'off', 'varnames', ...

{'subject','seconds'}, 'model', 'linear', 'contrasts', ...

'poly', 'dim', 2, 'posthoc', 'trt_vs_ctrl', 'nboot', 0);

% Ridge regression and bayesian analysis of posthoc comparisons

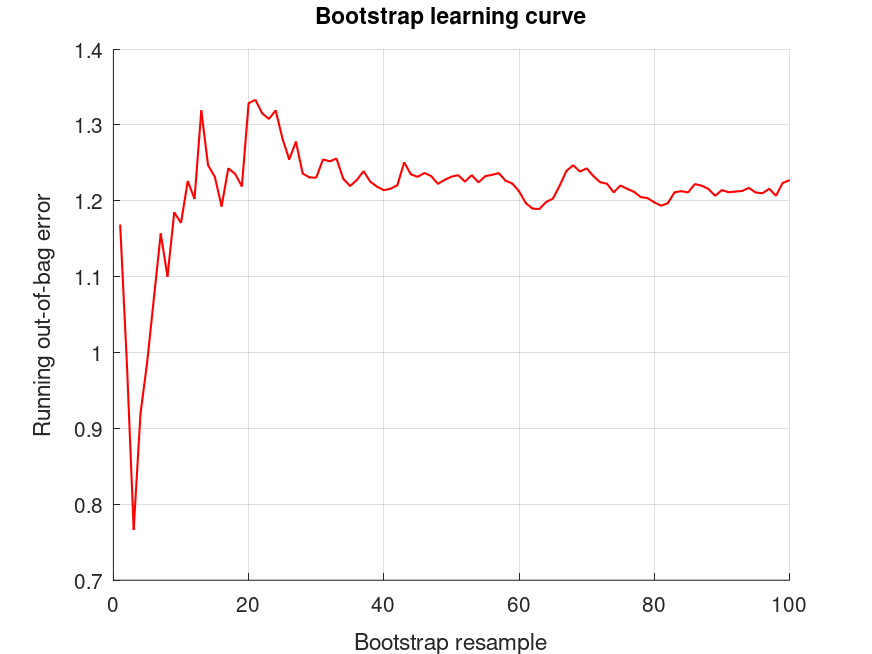

fprintf ('The bootridge function is running ...\n')

bootridge (MAT.Y, MAT.X, '*', 200, 0.05, MAT.L);

% Frequentist framework: wild bootstrap of linear model, with orthogonal

% polynomial contrast coding followed up estimating marginal means.

MAT = bootlm (words, {subject,seconds}, 'display', 'off', 'nboot', 0, ...

'model', 'linear', 'contrasts', 'poly', 'dim', 2);

% Ridge regression and bayesian analysis of model estimates. Note that group-

% mean Bayes Factors are NaN under the flat prior on the intercept whereas

% the contrasts we just calculated had proper Normal priors.

fprintf ('The bootridge function is running ...\n')

bootridge (MAT.Y, MAT.X, '*', 200, 0.05, MAT.L);

Produces the following output

The bootridge function is running ... Empirical Bayes Ridge Regression (.632 Bootstrap Tuning) - Summary ******************************************************************************* Number of predictors (p): 11 Number of outcomes (q): 1 Sample size: 30 Design effect (Deff): 1 Bootstrap resamples (nboot): 200 Minimized .632 bootstrap prediction error: 0.117537 Predicted R-squared: 0.882 (88.2%) Bootstrap optimized ridge tuning constant (lambda): 0.028454 Effective residual degrees of freedom (df_lambda): 18.1 Residual variance (sigma^2): 0.616 Inferential degrees of freedom (df_t): 18.1 Used for credible intervals and Bayes factors below. 95% credible intervals and Bayes factors for linear estimates. Global ridge prior contribution to posterior precision: 0.82 % Outcome 1: estimate CI_lower CI_upper lnBF10 prior +1.994 +1.258 +2.731 +6.86 t (0, 6.58, 18.1) +3.191 +2.455 +3.927 +13.5 t (0, 6.58, 18.1) The bootridge function is running ... Empirical Bayes Ridge Regression (.632 Bootstrap Tuning) - Summary ******************************************************************************* Number of predictors (p): 11 Number of outcomes (q): 1 Sample size: 30 Design effect (Deff): 1 Bootstrap resamples (nboot): 200 Minimized .632 bootstrap prediction error: 0.117537 Predicted R-squared: 0.882 (88.2%) Bootstrap optimized ridge tuning constant (lambda): 0.028454 Effective residual degrees of freedom (df_lambda): 18.1 Residual variance (sigma^2): 0.616 Inferential degrees of freedom (df_t): 18.1 Used for credible intervals and Bayes factors below. 95% credible intervals and Bayes factors for linear estimates. Global ridge prior contribution to posterior precision: 0.82 % Outcome 1: estimate CI_lower CI_upper lnBF10 prior +11.00 +10.48 +11.53 +NaN U (-Inf, Inf) +13.00 +12.48 +13.52 +NaN U (-Inf, Inf) +14.20 +13.67 +14.72 +NaN U (-Inf, Inf)

and the following figure

| Figure 1 |

|---|

|

Demonstration 4

The following code

% One-way design with continuous covariate. The data is from a study of the

% additive effects of species and temperature on chirpy pulses of crickets,

% from Stitch, The Worst Stats Text eveR

pulse = [67.9 65.1 77.3 78.7 79.4 80.4 85.8 86.6 87.5 89.1 ...

98.6 100.8 99.3 101.7 44.3 47.2 47.6 49.6 50.3 51.8 ...

60 58.5 58.9 60.7 69.8 70.9 76.2 76.1 77 77.7 84.7]';

temp = [20.8 20.8 24 24 24 24 26.2 26.2 26.2 26.2 28.4 ...

29 30.4 30.4 17.2 18.3 18.3 18.3 18.9 18.9 20.4 ...

21 21 22.1 23.5 24.2 25.9 26.5 26.5 26.5 28.6]';

species = {'ex' 'ex' 'ex' 'ex' 'ex' 'ex' 'ex' 'ex' 'ex' 'ex' 'ex' ...

'ex' 'ex' 'ex' 'niv' 'niv' 'niv' 'niv' 'niv' 'niv' 'niv' ...

'niv' 'niv' 'niv' 'niv' 'niv' 'niv' 'niv' 'niv' 'niv' 'niv'};

% Estimate regression coefficients using 'anova' contrast coding

MAT = bootlm (pulse, {temp, species}, 'model', 'linear', ...

'continuous', 1, 'display', 'off', ...

'contrasts', 'anova', 'nboot', 0);

% Ridge regression and bayesian analysis of regression coefficients

% MAT.X: column 1 is intercept, column 2 is temp (continuous), column 3

% is species (categorical).

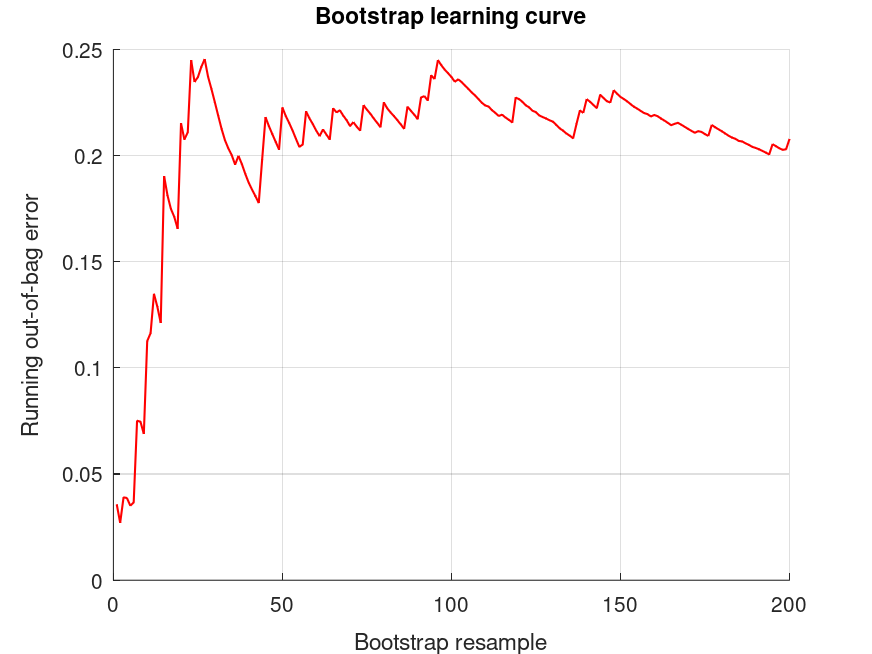

fprintf ('The bootridge function is running ...\n')

bootridge (MAT.Y, MAT.X, 3, 200, 0.05);

Produces the following output

The bootridge function is running ... Empirical Bayes Ridge Regression (.632 Bootstrap Tuning) - Summary ******************************************************************************* Number of predictors (p): 2 Number of outcomes (q): 1 Sample size: 31 Design effect (Deff): 1 Bootstrap resamples (nboot): 200 Minimized .632 bootstrap prediction error: 0.0122387 Predicted R-squared: 0.988 (98.8%) Bootstrap optimized ridge tuning constant (lambda): 0.0310279 Effective residual degrees of freedom (df_lambda): 28.0 Residual variance (sigma^2): 3.19 Inferential degrees of freedom (df_t): 28.0 Used for credible intervals and Bayes factors below. 95% credible intervals and Bayes factors for regression coefficients. Global ridge prior contribution to posterior precision: 0.33 % Stability selection (SS): >97.5% for the (-) or (+) sign of the coefficient. SS probabilities are reported in S.stability Outcome 1: coefficient CI_lower CI_upper lnBF10 SS prior +73.37 +72.71 +74.03 +NaN U (-Inf, Inf) +3.601 +3.402 +3.800 +53.4 (+) t (0, 2.65, 28.0) -10.03 -11.53 -8.528 +26.9 (-) t (0, 10.1, 28.0)

and the following figure

| Figure 1 |

|---|

|

Demonstration 5

The following code

% Variations in design for two-way ANOVA (2x2) with interaction.

% Arousal was measured in rodents assigned to four experimental groups in a

% between-subjects design with two factors: group (lesion/control) and

% stimulus (fearful/neutral). In this design, each rodent is allocated to one

% combination of levels in group and stimulus, and a single measurment of

% arousal is made. The question we are asking here is, does the effect of a

% fear-inducing stimulus on arousal depend on whether or not rodents had a

% lesion?

group = {'control' 'control' 'control' 'control' 'control' 'control' ...

'lesion' 'lesion' 'lesion' 'lesion' 'lesion' 'lesion' ...

'control' 'control' 'control' 'control' 'control' 'control' ...

'lesion' 'lesion' 'lesion' 'lesion' 'lesion' 'lesion'};

stimulus = {'fearful' 'fearful' 'fearful' 'fearful' 'fearful' 'fearful' ...

'fearful' 'fearful' 'fearful' 'fearful' 'fearful' 'fearful' ...

'neutral' 'neutral' 'neutral' 'neutral' 'neutral' 'neutral' ...

'neutral' 'neutral' 'neutral' 'neutral' 'neutral' 'neutral'};

arousal = [0.78 0.86 0.65 0.83 0.78 0.81 0.65 0.69 0.61 0.65 0.59 0.64 ...

0.54 0.6 0.67 0.63 0.56 0.55 0.645 0.565 0.625 0.485 0.655 0.515];

% Fit between-subjects design

[STATS, BOOTSTAT, AOVSTAT, PRED_ERR, MAT] = bootlm (arousal, ...

{group, stimulus}, 'seed', 1, ...

'display', 'off', 'contrasts', 'simple', ...

'model', 'full', ...

'method', 'bayes');

% Ridge regression and bayesian analysis of regression coefficients

% MAT.X: column 1 is intercept, column 2 is temp (continuous), column 3

% is species (categorical).

fprintf ('The bootridge function is running ...\n')

bootridge (MAT.Y, MAT.X, '*', 200, 0.05);

% Now imagine the design is repeated stimulus measurements in each rodent

ID = [1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12]';

% Fit model including ID as a blocking-factor

MAT = bootlm (arousal, {ID, group, stimulus}, 'seed', 1, 'nboot', 0, ...

'display', 'off', 'contrasts', 'simple', 'method', 'bayes', ...

'model', [1 0 0; 0 1 0; 0 0 1; 0 1 1]);

% Ridge regression and bayesian analysis of regression coefficients

% MAT.X: column 1 is intercept, column 2 is temp (continuous), column 3

% is species (categorical).

fprintf ('The bootridge function is running ...\n')

bootridge (MAT.Y, MAT.X, '*', 200, 0.05);

Produces the following output

The bootridge function is running ... Empirical Bayes Ridge Regression (.632 Bootstrap Tuning) - Summary ******************************************************************************* Number of predictors (p): 3 Number of outcomes (q): 1 Sample size: 24 Design effect (Deff): 1 Bootstrap resamples (nboot): 200 Minimized .632 bootstrap prediction error: 0.41427 Predicted R-squared: 0.586 (58.6%) Bootstrap optimized ridge tuning constant (lambda): 0.305249 Effective residual degrees of freedom (df_lambda): 20.3 Residual variance (sigma^2): 0.00356 Inferential degrees of freedom (df_t): 20.3 Used for credible intervals and Bayes factors below. 95% credible intervals and Bayes factors for regression coefficients. Global ridge prior contribution to posterior precision: 8.86 % Stability selection (SS): >97.5% for the (-) or (+) sign of the coefficient. SS probabilities are reported in S.stability Outcome 1: coefficient CI_lower CI_upper lnBF10 SS prior +0.6492 +0.6238 +0.6746 +NaN U (-Inf, Inf) -0.07454 -0.1241 -0.02501 +2.69 (-) t (0, 0.108, 20.3) -0.1189 -0.1685 -0.06942 +7.04 (-) t (0, 0.108, 20.3) +0.1136 +0.02100 +0.2061 +2.08 (+) t (0, 0.108, 20.3) The bootridge function is running ... Empirical Bayes Ridge Regression (.632 Bootstrap Tuning) - Summary ******************************************************************************* Number of predictors (p): 14 Number of outcomes (q): 1 Sample size: 24 Design effect (Deff): 1 Bootstrap resamples (nboot): 200 Minimized .632 bootstrap prediction error: 0.541584 Predicted R-squared: 0.458 (45.8%) Bootstrap optimized ridge tuning constant (lambda): 1.34378 Effective residual degrees of freedom (df_lambda): 15.2 Residual variance (sigma^2): 0.00422 Inferential degrees of freedom (df_t): 15.2 Used for credible intervals and Bayes factors below. 95% credible intervals and Bayes factors for regression coefficients. Global ridge prior contribution to posterior precision: 40.29 % Stability selection (SS): >97.5% for the (-) or (+) sign of the coefficient. SS probabilities are reported in S.stability Outcome 1: coefficient CI_lower CI_upper lnBF10 SS prior +0.6492 +0.6209 +0.6774 +NaN U (-Inf, Inf) +0.03475 -0.04703 +0.1165 +0.0470 t (0, 0.0561, 15.2) -0.007114 -0.08890 +0.07467 -0.359 t (0, 0.0561, 15.2) +0.03475 -0.04703 +0.1165 +0.0470 t (0, 0.0561, 15.2) -0.001133 -0.08292 +0.08065 -0.377 t (0, 0.0561, 15.2) +0.004848 -0.07694 +0.08663 -0.369 t (0, 0.0561, 15.2) +0.01436 -0.06856 +0.09729 -0.292 t (0, 0.0561, 15.2) +0.002400 -0.08053 +0.08533 -0.362 t (0, 0.0561, 15.2) -0.003582 -0.08651 +0.07934 -0.359 t (0, 0.0561, 15.2) -0.03349 -0.1164 +0.04944 +0.0206 t (0, 0.0561, 15.2) -0.0005911 -0.08352 +0.08233 -0.364 t (0, 0.0561, 15.2) -0.02751 -0.1104 +0.05542 -0.102 t (0, 0.0561, 15.2) -0.04841 -0.1174 +0.02057 +0.562 (-) t (0, 0.0561, 15.2) -0.1021 -0.1532 -0.05109 +5.52 (-) t (0, 0.0561, 15.2) +0.07209 -0.009930 +0.1541 +1.30 (+) t (0, 0.0561, 15.2)

and the following figure

| Figure 1 |

|---|

|

Demonstration 6

The following code

% Analysis of nested one-way design.

% Nested model example from:

% https://www.southampton.ac.uk/~cpd/anovas/datasets/#Chapter2

data = [4.5924 7.3809 21.322; -0.5488 9.2085 25.0426; ...

6.1605 13.1147 22.66; 2.3374 15.2654 24.1283; ...

5.1873 12.4188 16.5927; 3.3579 14.3951 10.2129; ...

6.3092 8.5986 9.8934; 3.2831 3.4945 10.0203];

clustid = [1 3 5; 1 3 5; 1 3 5; 1 3 5; ...

2 4 6; 2 4 6; 2 4 6; 2 4 6];

group = {'A' 'B' 'C'; 'A' 'B' 'C'; 'A' 'B' 'C'; 'A' 'B' 'C'; ...

'A' 'B' 'C'; 'A' 'B' 'C'; 'A' 'B' 'C'; 'A' 'B' 'C'};

% Fit model with cluster-based resampling. We are using Bayesian bootstrap

% using 'auto' prior, which effectively applies Bessel's correction to the

% variance of the bootstrap distribution for the contrasts (trt_vs_ctrl).

% Use 'treatment' coding and return regression coefficients since our

% intention is to use the posterior distributions from bayesian bootstrap

% to calculate the design effect.

[STATS, BOOTSTAT, AOVSTAT, PREDERR, MAT] = bootlm (data, {group}, ...

'clustid', clustid, 'seed', 1, 'display', 'off', 'contrasts', ...

'treatment', 'method', 'bayes', 'prior', 'auto');

% Or we can get a obtain the design effect empirically using resampling.

% We already fit the model accounting for clustering, now lets fit it

% under I.I.D. (i.e. without clustering). As above, use 'treatment' coding.

[STATS_SRS, BOOTSTAT_SRS] = bootlm (data, {group}, 'seed', 1, 'display', ...

'off', 'contrasts', 'treatment', 'method', 'bayes');

% Empirically calculate the design effect averaged over the variance of

% of the contrasts we are interested in

Var_true = var (BOOTSTAT, 0, 2);

Var_iid = var (BOOTSTAT_SRS, 0, 2);

DEFF = mean (Var_true ./ Var_iid);

% Or more simply, we can use the deffcalc function, which does the same thing.

% We take the mean DEFF across all contrasts for a stable global penalty.

DEFF = mean (deffcalc (BOOTSTAT, BOOTSTAT_SRS))

% Refit the model using orthogonal (helmert) contrasts and a hypothesis

% matrix specifying pairwise comparisons. Set nboot to 0 to avoid resampling.

MAT = bootlm (data, {group}, 'clustid', clustid, 'display', 'off', ...

'contrasts', 'helmert', 'dim', 1, 'posthoc', 'pairwise', ...

'nboot', 0);

% Fit a cluster-robust empirical Bayes model using our bootstrap estimate of

% the design effect and using the hypothesis matrix to define the comparisons

fprintf ('The bootridge function is running ...\n')

bootridge (MAT.Y, MAT.X, '*', 200, 0.05, MAT.L, DEFF);

% Compare this to using a maximum cluster size as an upperbound for Deff

g = max (accumarray (clustid(:), 1, [], @sum)); % g is max. cluster size

fprintf ('The bootridge function is running ...\n')

bootridge (MAT.Y, MAT.X, '*', 200, 0.05, MAT.L, g); % Upperbound DEFF is g

% Note: Using the empirical DEFF (~1.5) instead of the upper-bound (4.0)

% recovers inferential power, as seen by the higher Bayes Factor (lnBF10)

% and narrower credible intervals.

Produces the following output

DEFF = 1.4556 The bootridge function is running ... Empirical Bayes Ridge Regression (.632 Bootstrap Tuning) - Summary ******************************************************************************* Number of predictors (p): 2 Number of outcomes (q): 1 Sample size: 24 Design effect (Deff): 1.46 Bootstrap resamples (nboot): 200 Minimized .632 bootstrap prediction error: 0.463286 Predicted R-squared: 0.537 (53.7%) Bootstrap optimized ridge tuning constant (lambda, Deff-adjusted): 0.318356 Effective residual degrees of freedom (df_lambda): 21.1 Residual variance (sigma^2, Deff-inflated): 31.8 Inferential degrees of freedom (df_t, Deff-adjusted): 13.6 Used for credible intervals and Bayes factors below. 95% credible intervals and Bayes factors for linear estimates. Global ridge prior contribution to posterior precision: 6.50 % Outcome 1: estimate CI_lower CI_upper lnBF10 prior -6.336 -12.21 -0.4634 +1.03 t (0, 11.2, 13.6) -12.82 -18.69 -6.947 +5.63 t (0, 11.2, 13.6) -6.483 -12.32 -0.6518 +1.26 t (0, 9.99, 13.6) The bootridge function is running ... Empirical Bayes Ridge Regression (.632 Bootstrap Tuning) - Summary ******************************************************************************* Number of predictors (p): 2 Number of outcomes (q): 1 Sample size: 24 Design effect (Deff): 4 Bootstrap resamples (nboot): 200 Minimized .632 bootstrap prediction error: 0.463286 Predicted R-squared: 0.537 (53.7%) Bootstrap optimized ridge tuning constant (lambda, Deff-adjusted): 0.115848 Effective residual degrees of freedom (df_lambda): 21.0 Residual variance (sigma^2, Deff-inflated): 87.1 Inferential degrees of freedom (df_t, Deff-adjusted): 3.05 Used for credible intervals and Bayes factors below. 95% credible intervals and Bayes factors for linear estimates. Global ridge prior contribution to posterior precision: 2.47 % Outcome 1: estimate CI_lower CI_upper lnBF10 prior -6.532 -21.08 +8.017 -0.871 t (0, 30.7, 3.05) -13.33 -27.88 +1.214 +0.776 t (0, 30.7, 3.05) -6.802 -21.31 +7.708 -0.691 t (0, 27.4, 3.05)

and the following figure

| Figure 1 |

|---|

|

Demonstration 7

The following code

%% --- Stress-test: Simulated Large-Scale Patch-seq Project (bootridge) ---

%% N = 7500 cells

%% p = 15 features

%% q = 2000 genes

%% This tests memory handling and global lambda optimization.

N = 7500;

p = 15;

q = 2000;

nboot = 100;

% Set random seeds for the simulation

rand ('seed', 123);

randn ('seed', 123);

fprintf ('Simulate Large-Scale Patch-seq Dataset (%d x %d)...\n', N, q);

% Generate design matrix X (E-phys features)

X = [ones(N,1), randn(N, p-1)];

% Generate sparse multivariate outcome Y (Gene expression)

% Approx 120MB of data

true_beta = randn (p, q) .* (rand (p, q) > 0.9);

% Set signal-to-noise ratio to 0.5

target_snr = 0.5;

beta_no_intercept = true_beta(2:end, :);

signal_var_per_gene = sum (beta_no_intercept.^2, 1);

snr_per_gene = signal_var_per_gene / (0.5^2);

current_snr = mean (snr_per_gene);

scale = sqrt (target_snr / current_snr);

true_beta(2:end, :) = true_beta(2:end, :) * scale;

% Introduce correlations

n_factors = 10; % 10 latent biological processes

latent_X = randn (N, n_factors);

% Each latent factor affects about 10% of genes (sparse correlation)

latent_beta = randn (n_factors, q) .* (rand (n_factors, q) > 0.90);

% Simulate the data with added correlated noise (0.2 strength)

Y = X * true_beta + (latent_X * latent_beta * 0.2) + randn (N, q) * 0.5;

fprintf('Running bootridge ...\n');

tic;

% Use TOL = 0.05 for faster convergence in demo

S = bootridge (Y, X, [], nboot, 0.05, [], 1, 123, 0.05);

runtime = toc;

fprintf ('\n--- Performance Results ---\n');

fprintf ('Runtime: %.2f seconds\n', runtime);

fprintf ('Optimized Lambda: %.6f\n', S.lambda);

fprintf ('Total Iterations: %d\n', S.iter);

% Accuracy Check on a random gene

target_gene = ceil (rand * q);

estimated = S.coefficient(:, target_gene);

actual = true_beta(:, target_gene);

correlation = corr (estimated, actual);

% ROC statistics

threshold = 3; % corresponds to BF10 of 20

fp = sum (S.lnBF10(true_beta == 0) > threshold); % false positives

tp = sum (S.lnBF10(true_beta ~= 0) > threshold); % true positives

fn = sum (S.lnBF10(true_beta ~= 0) <= threshold); % missed true effects

power = tp / (tp + fn); % true positive rate

fp_rate = fp / sum (true_beta(:) == 0); % false positive rate

precision = tp / (tp + fp); % true discovery rate

fprintf ('Correlation of estimates for Gene %d: %.4f\n', ...

target_gene, correlation);

fprintf ('Number of coefficients: [%s] (Expected: [15 x 2000])\n', ...

num2str (size (S.coefficient)));

fprintf ('Number of pairwise correlations: [%s] (Expected: 1999000)\n', ...

num2str (size (S.RTAB, 1)));

fprintf ('Positive detections (i.e. discoveries) defined hereon as BF10 > 20');

fprintf ('\nFalse positive rate (FPR): %.1f%%\n', fp_rate * 100);

fprintf ('Precision (i.e. 1-FDR): %.1f%%\n', precision * 100);

fprintf ('Power (i.e. TPR): %.1f%%\n', power * 100);

Produces the following output

Simulate Large-Scale Patch-seq Dataset (7500 x 2000)... Running bootridge ... --- Performance Results --- Runtime: 893.60 seconds Optimized Lambda: 65.132264 Total Iterations: 12 Correlation of estimates for Gene 158: 0.9952 Number of coefficients: [15 2000] (Expected: [15 x 2000]) Number of pairwise correlations: [1999000] (Expected: 1999000) Positive detections (i.e. discoveries) defined hereon as BF10 > 20 False positive rate (FPR): 0.1% Precision (i.e. 1-FDR): 98.9% Power (i.e. TPR): 94.8%

Demonstration 8

The following code

%% --- Stress-test: Large-Scale Differential Gene Expression (DGE) Simulation ---

%% Scenario: Bulk RNA-seq Case-Control Study (e.g., Disease vs. Healthy)

%% N = 300 samples (e.g., 150 Patient / 150 Control)

%% p = 50 covariates (e.g., 1 Group Indicator + 49 Technical/PEER factors)

%% q = 15000 genes (Simultaneously modeled outcomes)

%%

%% This demo evaluates the multivariate efficiency of bootridge across

%% the typical protein-coding transcriptome size, testing memory handling

%% and the speed of global lambda optimization.

% 1. Setup Dimensions

N = 300; % Total biological samples (Bulk RNA-seq)

p = 50; % 1 Experimental Group + technical covariates (Age, RIN, Batch)

q = 15000; % Total Genes analyzed in this "chunk"

nboot = 100; % Number of bootstrap resamples

% Set random seeds for the simulation

rand ('seed', 123);

randn ('seed', 123);

fprintf (cat (2, 'Simulating DGE Dataset: %d samples, %d genes, %d ', ...

'covariates...\n'), N, q, p);

% 2. Generate Design Matrix X

% Column 1: Intercept

% Column 2: Group Indicator (0 = Control, 1 = Case)

% Columns 3-p: Random technical noise (Covariates/PEER factors)

Group = [zeros(N/2, 1); ones(N/2, 1)];

Covariates = randn (N, p-2);

X = [ones(N, 1), Group, Covariates];

% 3. Define Biological Signal (The "True" Log-Fold Changes)

% We simulate a realistic DGE profile:

% 10% of genes are differentially expressed (hits).

true_beta = zeros (p, q);

sig_genes = ceil (rand (1, round (q * 0.10)) * q);

true_beta(2, sig_genes) = (randn (1, length (sig_genes)) * 2); % Group effect

% 4. Generate Expression Matrix Y (Log2 TPM / Counts)

% Baseline + Group Effect + Gaussian noise.

Baseline = 5 + randn (1, q);

Y = repmat (Baseline, N, 1) + X * true_beta + randn (N, q) * 1.2;

fprintf ('Running Multivariate bootridge (Shrinkage shared across genes)...\n');

tic;

% CATEGOR = 2: Treats the Group column as categorical (no variance scaling).

% SEED = 123: Ensures reproducible bootstrap sampling.

% TOL = 0.05: Convergence tolerance for the golden section search.

S = bootridge (Y, X, 2, nboot, 0.05, [], 1, 123, 0.05);

runtime = toc;

% 5. Display Performance Results

fprintf ('\n--- Performance Results ---\n');

fprintf ('Runtime: %.2f seconds\n', runtime);

fprintf ('Optimized Lambda: %.6f\n', S.lambda);

% 6. Accuracy Check

% Compare estimated Beta (Group Effect) against the Ground Truth Fold-Changes

estimated_fc = S.coefficient(2, :);

true_fc = true_beta(2, :);

correlation = corr (estimated_fc', true_fc');

fprintf ('Correlation of Fold-Changes across %d genes: %.4f\n', ...

q, correlation);

fprintf ('Number of coefficients: [%s] (Expected: [50 x 15000])\n', ...

num2str (size (S.coefficient)));

fprintf ('Number of pairwise correlations: [%s] (Expected: 112492500)\n', ...

num2str (size (S.RTAB, 1)));

Produces the following output

Simulating DGE Dataset: 300 samples, 15000 genes, 50 covariates... Running Multivariate bootridge (Shrinkage shared across genes)... --- Performance Results --- Runtime: 483.80 seconds Optimized Lambda: 510.212731 Correlation of Fold-Changes across 15000 genes: 0.9759 Number of coefficients: [50 15000] (Expected: [50 x 15000]) Number of pairwise correlations: [112492500] (Expected: 112492500)

Demonstration 9

The following code

%% --- Stress-test: High-p Voxel-wise Neural Encoding Simulation ---

%% Scenario: Reconstructing Visual Stimuli from fMRI BOLD signals

%% N = 500 volumes (samples), p = 8000 voxels, q = 1 stimulus feature

%% This demo requires the signal package in octave

% 1. Setup Dimensions

N = 500; p = 8000; q = 1; nboot = 200;

rand ('seed', 123); randn ('seed', 123);

fprintf('Simulating fMRI Encoding: %d timepoints, %d voxels...\n', N, p);

% 2. Generate Design Matrix X (The Voxels)

% Spatial correlation between voxels (columns) and time points (rows)

X_raw = randn (N, p-1);

X = [ones(N, 1), filter([0.5 1 0.5], 1, X_raw, [], 2)];

X(:,2:end) = filter ([0.1, 0.4, 0.9, 1, 0.6, 0.2], 1, X(:,2:end), [], 1);

% 3. Define the "Neural Code" (True Weights)

true_beta_sparse = zeros (p, q); % Initialise

active_voxels = 1 + ceil (rand (1, 25) * (p - 1)); % 50 spatial clusters

true_beta_sparse(active_voxels) = randn (25, 1) * 100; % Active voxels

kernel = [0.05 0.1 0.4 0.8 1 0.8 0.4 0.1 0.05]; % Smoothing kernel

true_beta = filter (kernel, 1, true_beta_sparse); % Smooth active voxels

% 4. Generate outcome Y (The Stimulus)

% Signal from smoothed clusters + Gaussian noise

Y = X * true_beta + randn (N, q);

% 5. Estimate Design Effect (Deff) to account for serial dependence

% We use the autocorrelation of Y to estimate the variance inflation factor

%

% Bayley, G. V., & Hammersley, J. M. (1946). The "Effective" Number of

% Independent Observations in an Autocorrelated Time Series. Supplement to

% the Journal of the Royal Statistical Society, 8(2), 184–197.

% https://doi.org/10.2307/2983560

try

info = ver;

isoctave = any (ismember ({info.Name}, 'Octave'));

if (isoctave)

pkg load signal;

end

[r, lags] = xcov (Y - mean (Y), 10, 'coeff');

Deff = 1 + 2 * sum (r(lags > 0));

fprintf ('Estimated Design Effect (Deff): %.3f\n', Deff);

catch

Deff = 1;

end

% 6. Run bootridge

fprintf ('Running bootridge (Global Lambda Optimization)...\n');

tic;

% Run the bootridge function

S = bootridge (Y, X, [], nboot, 0.05, [], Deff, 123, 0.05);

runtime = toc;

% 7. Performance Results

estimated_beta = S.coefficient;

correlation = corr (estimated_beta, true_beta);

fprintf ('\n--- Performance Results ---\n');

fprintf ('Runtime: %.2f seconds\n', runtime);

fprintf ('Optimized Lambda: %.6f\n', S.lambda);

fprintf ('Correlation of Voxel Weight Map: %.4f\n', correlation);

fprintf ('Number of coefficients: [%s] (Expected: [8000 x 1])\n', ...

num2str (size (S.coefficient)));

Produces the following output

Simulating fMRI Encoding: 500 timepoints, 8000 voxels... Estimated Design Effect (Deff): 3.489 Running bootridge (Global Lambda Optimization)... Note: t-statistics evaluated with effective degrees of freedom clamped at 1 degree of freedom. --- Performance Results --- Runtime: 1713.78 seconds Optimized Lambda: 0.326447 Correlation of Voxel Weight Map: 0.3970 Number of coefficients: [8000 1] (Expected: [8000 x 1])

Demonstration 10

The following code

% Error Control: Global Ridge vs Per-Outcome Wild Bootstrap (n = 40)

% under global multicollinearity (r = 0.2)

%

% --- Parameters ---

% n_sims = 30;

% alpha = 0.05;

% n_vals = 40;

% p_vals = [3, 10, 30];

% q_vals = [1, 5, 10];

% snr_vals = [0.1, 0.2, 0.4, 0.8];

% seed = 42;

% randn('seed', seed);

%

% for p = p_vals

% for q = q_vals

% for snr = snr_vals

% % Accumulators

% fpr_r_ci = 0; fpr_r_bf = 0; fpr_r_ss = 0;

% fpr_w_std = 0; fpr_w_max = 0;

% fdr_r_ci = 0; fdr_r_bf = 0; fdr_r_ss = 0;

% fdr_w_std = 0; fdr_w_max = 0;

% pow_r_ci = 0; pow_r_bf = 0; pow_r_ss = 0;

% pow_w_std = 0; pow_w_max = 0;

% sig_hits_r = 0; type_s_r = 0; type_m_r = 0;

% sig_hits_w = 0; type_s_w = 0; type_m_w = 0;

% mse_r = 0; mse_w = 0;

%

% for s = 1:n_sims

% % 1. Induce Predictor Correlation (r = 0.2)

% X_raw = randn(n_vals, p);

% X = bsxfun(@plus, X_raw * 0.8944, randn(n_vals, 1) * 0.4472);

% X = [ones(n_vals, 1), X];

%

% % 2. Setup Signal (Variable 2 is the only true signal)

% beta_true = zeros(p+1, q);

% beta_true(2, :) = snr;

%

% % 3. Induce Outcome Noise Correlation (r = 0.2)

% noise_unique = randn(n_vals, q);

% noise_common = randn(n_vals, 1);

% E = bsxfun(@plus, noise_unique * 0.8944, noise_common * 0.4472);

%

% % 4. Generate Y

% y_raw = X * beta_true + E;

% y = (y_raw - mean(y_raw)) ./ std(y_raw);

%

% S_r = bootridge(y, X, [], 200, alpha, [], 1, s);

%

% rej_w_std = false(p+1, q);

% rej_w_max = false(p+1, q);

% coeffs_w = zeros(p+1, q);

% for j = 1:q

% res_std = bootwild(y(:,j), X, [], 1999, alpha, s, 0);

% res_max = bootwild(y(:,j), X, [], 1999, {alpha}, s, 1);

% rej_w_std(:, j) = (res_std.pval <= alpha);

% rej_w_max(:, j) = (res_max.pval <= alpha);

% coeffs_w(:, j) = res_max.original;

% end

%

% % --- Indices ---

% null_idx = 3:(p+1);

% sig_idx = 2;

%

% % --- Ridge Decisions ---

% dec_r_ci = (S_r.CI_lower > 0 | S_r.CI_upper < 0);

% dec_r_bf = (S_r.lnBF10 >= 1);

% dec_r_ss = (S_r.stability > (1 - alpha/2));

%

% % --- FDR Calculation ---

% fd = sum(sum(dec_r_ci(null_idx, :)));

% td = sum(sum(dec_r_ci(2:(p+1), :)));

% if td > 0, fdr_r_ci = fdr_r_ci + (fd/td); end

%

% fd = sum(sum(dec_r_bf(null_idx, :)));

% td = sum(sum(dec_r_bf(2:(p+1), :)));

% if td > 0, fdr_r_bf = fdr_r_bf + (fd/td); end

%

% fd = sum(sum(dec_r_ss(null_idx, :)));

% td = sum(sum(dec_r_ss(2:(p+1), :)));

% if td > 0, fdr_r_ss = fdr_r_ss + (fd/td); end

%

% fd = sum(sum(rej_w_std(null_idx, :)));

% td = sum(sum(rej_w_std(2:(p+1), :)));

% if td > 0, fdr_w_std = fdr_w_std + (fd/td); end

%

% fd = sum(sum(rej_w_max(null_idx, :)));

% td = sum(sum(rej_w_max(2:(p+1), :)));

% if td > 0, fdr_w_max = fdr_w_max + (fd/td); end

%

% % --- FPR ---

% num_null_total = length(null_idx) * q;

% fpr_r_ci = fpr_r_ci + (sum(sum(dec_r_ci(null_idx, :))) / ...

% num_null_total);

% fpr_r_bf = fpr_r_bf + (sum(sum(dec_r_bf(null_idx, :))) / ...

% num_null_total);

% fpr_r_ss = fpr_r_ss + (sum(sum(dec_r_ss(null_idx, :))) / ...

% num_null_total);

% fpr_w_std = fpr_w_std + (sum(sum(rej_w_std(null_idx, :))) / ...

% num_null_total);

% fpr_w_max = fpr_w_max + (sum(sum(rej_w_max(null_idx, :))) / ...

% num_null_total);

%

% % --- Signal Analysis ---

% pow_r_ci = pow_r_ci + (sum(dec_r_ci(sig_idx, :)) / q);

% pow_r_bf = pow_r_bf + (sum(dec_r_bf(sig_idx, :)) / q);

% pow_r_ss = pow_r_ss + (sum(dec_r_ss(sig_idx, :)) / q);

% pow_w_std = pow_w_std + (sum(rej_w_std(sig_idx, :)) / q);

% pow_w_max = pow_w_max + (sum(rej_w_max(sig_idx, :)) / q);

%

% for j = 1:q

% if dec_r_ci(sig_idx, j)

% sig_hits_r = sig_hits_r + 1;

% if sign(S_r.coefficient(2,j)) ~= sign(snr)

% type_s_r = type_s_r + 1;

% end

% type_m_r = type_m_r + (abs(S_r.coefficient(2,j)) / abs(snr));

% end

% if rej_w_max(sig_idx, j)

% sig_hits_w = sig_hits_w + 1;

% if sign(coeffs_w(2,j)) ~= sign(snr)

% type_s_w = type_s_w + 1;

% end

% type_m_w = type_m_w + (abs(coeffs_w(2,j)) / abs(snr));

% end

% end

%

% X_test = [ones(50, 1), randn(50, p)];

% y_test_raw = X_test * beta_true + randn(50, q);

% y_test = (y_test_raw - mean(y_test_raw)) ./ std(y_test_raw);

% mse_r = mse_r + mean(mean((y_test - X_test*S_r.coefficient).^2));

% mse_w = mse_w + mean(mean((y_test - X_test*coeffs_w).^2));

% end

%

% end

% end

% end

%

% | |--- MSE ---|

% Cond (p,q) | SNR |Ridge Wild

% ------------------------------|

% p3 q1 | 0.1 |1.00 1.07 |

% p3 q1 | 0.2 |0.98 1.04 |

% p3 q1 | 0.4 |0.90 0.91 |

% p3 q1 | 0.8 |0.68 0.69 |

% ------------------------------|

% p3 q5 | 0.1 |0.99 1.06 |

% p3 q5 | 0.2 |0.97 1.03 |

% p3 q5 | 0.4 |0.90 0.94 |

% p3 q5 | 0.8 |0.68 0.70 |

% ------------------------------|

% p3 q10 | 0.1 |0.99 1.07 |

% p3 q10 | 0.2 |0.97 1.03 |

% p3 q10 | 0.4 |0.90 0.94 |

% p3 q10 | 0.8 |0.66 0.67 |

% ------------------------------|

% p10 q1 | 0.1 |1.01 1.38 |

% p10 q1 | 0.2 |1.02 1.39 |

% p10 q1 | 0.4 |0.98 1.24 |

% p10 q1 | 0.8 |0.77 0.85 |

% ------------------------------|

% p10 q5 | 0.1 |1.00 1.37 |

% p10 q5 | 0.2 |0.99 1.35 |

% p10 q5 | 0.4 |0.94 1.21 |

% p10 q5 | 0.8 |0.75 0.88 |

% ------------------------------|

% p10 q10 | 0.1 |1.00 1.42 |

% p10 q10 | 0.2 |0.99 1.36 |

% p10 q10 | 0.4 |0.95 1.25 |

% p10 q10 | 0.8 |0.74 0.87 |

% ------------------------------|

% p30 q1 | 0.1 |1.13 5.49 |

% p30 q1 | 0.2 |1.07 5.02 |

% p30 q1 | 0.4 |1.05 4.51 |

% p30 q1 | 0.8 |0.94 3.20 |

% ------------------------------|

% p30 q5 | 0.1 |1.07 5.36 |

% p30 q5 | 0.2 |1.04 5.34 |

% p30 q5 | 0.4 |1.04 4.39 |

% p30 q5 | 0.8 |0.90 3.58 |

% ------------------------------|

% p30 q10 | 0.1 |1.04 5.95 |

% p30 q10 | 0.2 |1.05 5.71 |

% p30 q10 | 0.4 |1.02 4.86 |

% p30 q10 | 0.8 |0.87 3.18 |

% ------------------------------|

% | |--- Ridge Pow --- | Wild Pow |

% Cond (p,q) | SNR |CI BF SS | Std MaxT |

% ---------------------------------------------------|

% p3 q1 | 0.1 |0.10 0.13 0.17 | 0.13 0.07 |

% p3 q1 | 0.2 |0.07 0.10 0.20 | 0.20 0.10 |

% p3 q1 | 0.4 |0.30 0.40 0.60 | 0.47 0.23 |

% p3 q1 | 0.8 |0.97 1.00 1.00 | 1.00 0.90 |

% ---------------------------------------------------|

% p3 q5 | 0.1 |0.00 0.01 0.09 | 0.09 0.01 |

% p3 q5 | 0.2 |0.10 0.15 0.32 | 0.23 0.12 |

% p3 q5 | 0.4 |0.39 0.57 0.70 | 0.61 0.35 |

% p3 q5 | 0.8 |1.00 1.00 1.00 | 0.99 0.97 |

% ---------------------------------------------------|

% p3 q10 | 0.1 |0.02 0.07 0.12 | 0.10 0.05 |

% p3 q10 | 0.2 |0.08 0.15 0.29 | 0.23 0.10 |

% p3 q10 | 0.4 |0.50 0.62 0.68 | 0.64 0.49 |

% p3 q10 | 0.8 |0.95 0.97 0.97 | 0.95 0.89 |

% ---------------------------------------------------|

% p10 q1 | 0.1 |0.03 0.07 0.20 | 0.13 0.00 |

% p10 q1 | 0.2 |0.03 0.03 0.17 | 0.07 0.03 |

% p10 q1 | 0.4 |0.23 0.43 0.53 | 0.43 0.13 |

% p10 q1 | 0.8 |0.90 0.97 1.00 | 0.97 0.83 |

% ---------------------------------------------------|

% p10 q5 | 0.1 |0.02 0.05 0.14 | 0.10 0.01 |

% p10 q5 | 0.2 |0.02 0.07 0.28 | 0.19 0.05 |

% p10 q5 | 0.4 |0.29 0.50 0.65 | 0.47 0.23 |

% p10 q5 | 0.8 |0.94 0.97 0.99 | 0.97 0.82 |

% ---------------------------------------------------|

% p10 q10 | 0.1 |0.00 0.00 0.09 | 0.07 0.00 |

% p10 q10 | 0.2 |0.01 0.06 0.24 | 0.15 0.02 |

% p10 q10 | 0.4 |0.29 0.46 0.71 | 0.51 0.23 |

% p10 q10 | 0.8 |0.94 0.98 0.99 | 0.96 0.79 |

% ---------------------------------------------------|

% p30 q1 | 0.1 |0.00 0.00 0.10 | 0.00 0.00 |

% p30 q1 | 0.2 |0.00 0.03 0.17 | 0.13 0.03 |

% p30 q1 | 0.4 |0.17 0.30 0.67 | 0.17 0.03 |

% p30 q1 | 0.8 |0.83 0.90 1.00 | 0.57 0.10 |

% ---------------------------------------------------|

% p30 q5 | 0.1 |0.01 0.02 0.15 | 0.11 0.02 |

% p30 q5 | 0.2 |0.00 0.01 0.23 | 0.09 0.01 |

% p30 q5 | 0.4 |0.13 0.33 0.71 | 0.25 0.07 |

% p30 q5 | 0.8 |0.71 0.87 0.98 | 0.45 0.17 |

% ---------------------------------------------------|

% p30 q10 | 0.1 |0.00 0.00 0.15 | 0.11 0.01 |

% p30 q10 | 0.2 |0.01 0.06 0.27 | 0.11 0.01 |

% p30 q10 | 0.4 |0.05 0.22 0.57 | 0.17 0.02 |

% p30 q10 | 0.8 |0.74 0.89 0.97 | 0.54 0.15 |

% ---------------------------------------------------|

% | |Ridge Errors | Wild Errors |

% Cond (p,q) | SNR |TypeS TypeM | TypeS TypeM |

% -------------------------------------------------|

% p3 q1 | 0.1 |0.333 3.53 | 0.500 4.89 |

% p3 q1 | 0.2 |0.000 2.02 | 0.000 2.47 |

% p3 q1 | 0.4 |0.000 0.86 | 0.000 1.17 |

% p3 q1 | 0.8 |0.000 0.66 | 0.000 0.79 |

% -------------------------------------------------|

% p3 q5 | 0.1 |0.000 ND | 0.000 3.42 |

% p3 q5 | 0.2 |0.000 1.29 | 0.000 2.15 |

% p3 q5 | 0.4 |0.000 0.80 | 0.000 1.23 |

% p3 q5 | 0.8 |0.000 0.70 | 0.000 0.81 |

% -------------------------------------------------|

% p3 q10 | 0.1 |0.000 2.55 | 0.067 4.27 |

% p3 q10 | 0.2 |0.000 1.33 | 0.000 2.46 |

% p3 q10 | 0.4 |0.000 0.82 | 0.000 1.19 |

% p3 q10 | 0.8 |0.000 0.67 | 0.000 0.81 |

% -------------------------------------------------|

% p10 q1 | 0.1 |0.000 1.90 | 0.000 0.00 |

% p10 q1 | 0.2 |0.000 1.49 | 0.000 2.51 |

% p10 q1 | 0.4 |0.000 0.84 | 0.000 1.47 |

% p10 q1 | 0.8 |0.000 0.54 | 0.000 0.82 |

% -------------------------------------------------|

% p10 q5 | 0.1 |0.000 2.36 | 0.000 6.21 |

% p10 q5 | 0.2 |0.000 1.10 | 0.000 2.83 |

% p10 q5 | 0.4 |0.000 0.65 | 0.000 1.38 |

% p10 q5 | 0.8 |0.000 0.57 | 0.000 0.86 |

% -------------------------------------------------|

% p10 q10 | 0.1 |0.000 ND | 0.000 ND |

% p10 q10 | 0.2 |0.000 1.05 | 0.000 2.54 |

% p10 q10 | 0.4 |0.000 0.69 | 0.000 1.47 |

% p10 q10 | 0.8 |0.000 0.52 | 0.000 0.84 |

% -------------------------------------------------|

% p30 q1 | 0.1 |0.000 ND | 0.000 ND |

% p30 q1 | 0.2 |0.000 ND | 0.000 4.21 |

% p30 q1 | 0.4 |0.000 0.74 | 0.000 3.27 |

% p30 q1 | 0.8 |0.000 0.39 | 0.000 1.38 |

% -------------------------------------------------|

% p30 q5 | 0.1 |0.000 3.28 | 0.000 10.07 |

% p30 q5 | 0.2 |0.000 ND | 0.000 3.71 |

% p30 q5 | 0.4 |0.000 0.59 | 0.000 1.88 |

% p30 q5 | 0.8 |0.000 0.37 | 0.000 1.09 |

% -------------------------------------------------|

% p30 q10 | 0.1 |0.000 ND | 0.000 8.19 |

% p30 q10 | 0.2 |0.000 1.16 | 0.000 5.66 |

% p30 q10 | 0.4 |0.000 0.58 | 0.000 2.61 |

% p30 q10 | 0.8 |0.000 0.39 | 0.000 1.05 |

% -------------------------------------------------|

% | |--- Ridge FPR --- | Wild FPR |

% Cond (p,q) | SNR |CI BF SS | Std MaxT |

% ---------------------------------------------------|

% p3 q1 | 0.1 |0.000 0.000 0.000 | 0.017 0.000 |

% p3 q1 | 0.2 |0.000 0.033 0.050 | 0.017 0.000 |

% p3 q1 | 0.4 |0.017 0.017 0.033 | 0.067 0.017 |

% p3 q1 | 0.8 |0.033 0.050 0.083 | 0.050 0.017 |

% ---------------------------------------------------|

% p3 q5 | 0.1 |0.003 0.023 0.077 | 0.050 0.027 |

% p3 q5 | 0.2 |0.010 0.030 0.093 | 0.067 0.017 |

% p3 q5 | 0.4 |0.040 0.060 0.093 | 0.080 0.027 |

% p3 q5 | 0.8 |0.023 0.023 0.040 | 0.050 0.003 |

% ---------------------------------------------------|

% p3 q10 | 0.1 |0.008 0.025 0.075 | 0.073 0.023 |

% p3 q10 | 0.2 |0.002 0.015 0.052 | 0.047 0.007 |

% p3 q10 | 0.4 |0.025 0.048 0.088 | 0.078 0.037 |

% p3 q10 | 0.8 |0.048 0.050 0.077 | 0.067 0.038 |

% ---------------------------------------------------|

% p10 q1 | 0.1 |0.004 0.019 0.085 | 0.059 0.004 |

% p10 q1 | 0.2 |0.011 0.019 0.074 | 0.067 0.004 |

% p10 q1 | 0.4 |0.019 0.033 0.085 | 0.063 0.015 |

% p10 q1 | 0.8 |0.022 0.037 0.052 | 0.063 0.007 |

% ---------------------------------------------------|

% p10 q5 | 0.1 |0.000 0.004 0.065 | 0.066 0.005 |

% p10 q5 | 0.2 |0.001 0.009 0.070 | 0.071 0.004 |

% p10 q5 | 0.4 |0.004 0.016 0.073 | 0.058 0.010 |

% p10 q5 | 0.8 |0.024 0.046 0.073 | 0.075 0.010 |

% ---------------------------------------------------|

% p10 q10 | 0.1 |0.000 0.005 0.065 | 0.066 0.007 |

% p10 q10 | 0.2 |0.001 0.009 0.068 | 0.059 0.008 |

% p10 q10 | 0.4 |0.006 0.024 0.073 | 0.067 0.009 |

% p10 q10 | 0.8 |0.016 0.037 0.071 | 0.072 0.008 |

% ---------------------------------------------------|

% p30 q1 | 0.1 |0.002 0.017 0.084 | 0.070 0.007 |

% p30 q1 | 0.2 |0.009 0.014 0.083 | 0.074 0.009 |

% p30 q1 | 0.4 |0.001 0.013 0.079 | 0.052 0.001 |

% p30 q1 | 0.8 |0.009 0.021 0.078 | 0.069 0.008 |

% ---------------------------------------------------|

% p30 q5 | 0.1 |0.002 0.008 0.090 | 0.088 0.006 |

% p30 q5 | 0.2 |0.001 0.006 0.077 | 0.077 0.008 |

% p30 q5 | 0.4 |0.003 0.015 0.089 | 0.076 0.003 |

% p30 q5 | 0.8 |0.005 0.024 0.094 | 0.094 0.010 |

% ---------------------------------------------------|

% p30 q10 | 0.1 |0.001 0.005 0.077 | 0.086 0.007 |

% p30 q10 | 0.2 |0.001 0.005 0.084 | 0.089 0.010 |

% p30 q10 | 0.4 |0.000 0.010 0.083 | 0.081 0.004 |

% p30 q10 | 0.8 |0.005 0.024 0.089 | 0.084 0.006 |

% ---------------------------------------------------|

% | |------ Ridge FDR ------ | Wild FDR |

% Cond (p,q) | SNR |FD-CI FD-BF FD-SS | Std MaxT |

% ---------------------------------------------------------|

% p3 q1 | 0.1 |0.000 0.000 0.000 | 0.033 0.000 |

% p3 q1 | 0.2 |0.000 0.067 0.083 | 0.033 0.000 |

% p3 q1 | 0.4 |0.017 0.017 0.050 | 0.083 0.017 |

% p3 q1 | 0.8 |0.033 0.050 0.083 | 0.050 0.017 |

% ---------------------------------------------------------|

% p3 q5 | 0.1 |0.033 0.183 0.450 | 0.356 0.217 |

% p3 q5 | 0.2 |0.083 0.178 0.367 | 0.367 0.119 |

% p3 q5 | 0.4 |0.116 0.145 0.178 | 0.173 0.086 |

% p3 q5 | 0.8 |0.036 0.034 0.060 | 0.074 0.007 |

% ---------------------------------------------------------|

% p3 q10 | 0.1 |0.140 0.241 0.551 | 0.501 0.271 |

% p3 q10 | 0.2 |0.008 0.117 0.304 | 0.282 0.069 |

% p3 q10 | 0.4 |0.088 0.130 0.194 | 0.188 0.122 |

% p3 q10 | 0.8 |0.081 0.083 0.127 | 0.111 0.076 |

% ---------------------------------------------------------|

% p10 q1 | 0.1 |0.033 0.133 0.456 | 0.383 0.033 |

% p10 q1 | 0.2 |0.100 0.150 0.522 | 0.422 0.033 |

% p10 q1 | 0.4 |0.106 0.206 0.461 | 0.372 0.100 |

% p10 q1 | 0.8 |0.089 0.156 0.211 | 0.256 0.033 |

% ---------------------------------------------------------|

% p10 q5 | 0.1 |0.000 0.092 0.788 | 0.848 0.200 |

% p10 q5 | 0.2 |0.050 0.200 0.709 | 0.771 0.122 |