Categories &

Functions List

- BetaDistribution

- BinomialDistribution

- BirnbaumSaundersDistribution

- BurrDistribution

- ExponentialDistribution

- ExtremeValueDistribution

- GammaDistribution

- GeneralizedExtremeValueDistribution

- GeneralizedParetoDistribution

- HalfNormalDistribution

- InverseGaussianDistribution

- LogisticDistribution

- LoglogisticDistribution

- LognormalDistribution

- LoguniformDistribution

- MultinomialDistribution

- NakagamiDistribution

- NegativeBinomialDistribution

- NormalDistribution

- PiecewiseLinearDistribution

- PoissonDistribution

- RayleighDistribution

- RicianDistribution

- tLocationScaleDistribution

- TriangularDistribution

- UniformDistribution

- WeibullDistribution

- betafit

- betalike

- binofit

- binolike

- bisafit

- bisalike

- burrfit

- burrlike

- evfit

- evlike

- expfit

- explike

- gamfit

- gamlike

- geofit

- gevfit_lmom

- gevfit

- gevlike

- gpfit

- gplike

- gumbelfit

- gumbellike

- hnfit

- hnlike

- invgfit

- invglike

- logifit

- logilike

- loglfit

- logllike

- lognfit

- lognlike

- nakafit

- nakalike

- nbinfit

- nbinlike

- normfit

- normlike

- poissfit

- poisslike

- raylfit

- rayllike

- ricefit

- ricelike

- tlsfit

- tlslike

- unidfit

- unifit

- wblfit

- wbllike

- betacdf

- betainv

- betapdf

- betarnd

- binocdf

- binoinv

- binopdf

- binornd

- bisacdf

- bisainv

- bisapdf

- bisarnd

- burrcdf

- burrinv

- burrpdf

- burrrnd

- bvncdf

- bvtcdf

- cauchycdf

- cauchyinv

- cauchypdf

- cauchyrnd

- chi2cdf

- chi2inv

- chi2pdf

- chi2rnd

- copulacdf

- copulapdf

- copularnd

- evcdf

- evinv

- evpdf

- evrnd

- expcdf

- expinv

- exppdf

- exprnd

- fcdf

- finv

- fpdf

- frnd

- gamcdf

- gaminv

- gampdf

- gamrnd

- geocdf

- geoinv

- geopdf

- geornd

- gevcdf

- gevinv

- gevpdf

- gevrnd

- gpcdf

- gpinv

- gppdf

- gprnd

- gumbelcdf

- gumbelinv

- gumbelpdf

- gumbelrnd

- hncdf

- hninv

- hnpdf

- hnrnd

- hygecdf

- hygeinv

- hygepdf

- hygernd

- invgcdf

- invginv

- invgpdf

- invgrnd

- iwishpdf

- iwishrnd

- jsucdf

- jsupdf

- laplacecdf

- laplaceinv

- laplacepdf

- laplacernd

- logicdf

- logiinv

- logipdf

- logirnd

- loglcdf

- loglinv

- loglpdf

- loglrnd

- logncdf

- logninv

- lognpdf

- lognrnd

- mnpdf

- mnrnd

- mvncdf

- mvnpdf

- mvnrnd

- mvtcdf

- mvtpdf

- mvtrnd

- mvtcdfqmc

- nakacdf

- nakainv

- nakapdf

- nakarnd

- nbincdf

- nbininv

- nbinpdf

- nbinrnd

- ncfcdf

- ncfinv

- ncfpdf

- ncfrnd

- nctcdf

- nctinv

- nctpdf

- nctrnd

- ncx2cdf

- ncx2inv

- ncx2pdf

- ncx2rnd

- normcdf

- norminv

- normpdf

- normrnd

- plcdf

- plinv

- plpdf

- plrnd

- poisscdf

- poissinv

- poisspdf

- poissrnd

- raylcdf

- raylinv

- raylpdf

- raylrnd

- ricecdf

- riceinv

- ricepdf

- ricernd

- tcdf

- tinv

- tpdf

- trnd

- tlscdf

- tlsinv

- tlspdf

- tlsrnd

- tricdf

- triinv

- tripdf

- trirnd

- unidcdf

- unidinv

- unidpdf

- unidrnd

- unifcdf

- unifinv

- unifpdf

- unifrnd

- vmcdf

- vminv

- vmpdf

- vmrnd

- wblcdf

- wblinv

- wblpdf

- wblrnd

- wienrnd

- wishpdf

- wishrnd

- adtest

- anova

- anova1

- anova2

- anovan

- bartlett_test

- barttest

- binotest

- chi2gof

- chi2test

- correlation_test

- fishertest

- friedman

- hotelling_t2test

- hotelling_t2test2

- kruskalwallis

- kstest

- kstest2

- levene_test

- manova1

- mcnemar_test

- multcompare

- ranksum

- regression_ftest

- regression_ttest

- runstest

- sampsizepwr

- signrank

- signtest

- tiedrank

- ttest

- ttest2

- vartest

- vartest2

- vartestn

- ztest

- ztest2

Class Definition: GeneralizedParetoDistribution

statistics: GeneralizedParetoDistribution

Generalized Pareto probability distribution object.

A GeneralizedParetoDistribution object consists of parameters, a

model description, and sample data for a Generalized Pareto probability

distribution.

The Generalized Pareto distribution is a continuous probability distribution that models the tail behavior of other distributions, commonly used for extreme value analysis. It is defined by shape parameter k, scale parameter sigma, and location parameter theta.

There are several ways to create a GeneralizedParetoDistribution

object.

- Fit a distribution to data using the

fitdistfunction. - Create a distribution with fixed parameter values using the

makedistfunction. - Use the constructor

GeneralizedParetoDistribution (k, sigma, theta)to create a Generalized Pareto distribution with fixed parameter values k, sigma, and theta. - Use the static method

GeneralizedParetoDistribution.fit (x, theta, alpha, freq, options)to fit a distribution to the data in x using the same input arguments as thegpfitfunction.

It is highly recommended to use fitdist and makedist

functions to create probability distribution objects, instead of the class

constructor or the aforementioned static method.

Further information about the Generalized Pareto distribution can be found at https://en.wikipedia.org/wiki/Generalized_Pareto_distribution

See also: fitdist, makedist, gpcdf, gpinv, gppdf, gprnd, gpfit, gplike, gpstat

Source Code: GeneralizedParetoDistribution

The GeneralizedParetoDistribution class contains the following properties:

A scalar value characterizing the shape of the Generalized Pareto

distribution. You can access the k property using dot name

assignment.

Example: 1

Create a Generalized Pareto distribution with default parameters

pd = makedist ("GeneralizedPareto")

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 1

sigma = 1

theta = 1

Query parameter 'k' (shape parameter)

pd.k

ans = 1

Set parameter 'k'

pd.k = 0.5

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 1

Use this to initialize or modify the shape parameter of a Generalized Pareto distribution. The shape parameter can be any real scalar and determines the tail behavior (heavy-tailed if k>0).

Example: 2

Create a Generalized Pareto distribution object by calling its constructor

pd = GeneralizedParetoDistribution (0.5, 1, 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

Query parameter 'k'

pd.k

ans = 0.5000

This demonstrates direct construction with a specific shape parameter, useful for modeling extreme values with known tail index.

A positive scalar value characterizing the scale of the Generalized

Pareto distribution. You can access the sigma property using dot

name assignment.

Example: 1

Create a Generalized Pareto distribution with default parameters

pd = makedist ("GeneralizedPareto")

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 1

sigma = 1

theta = 1

Query parameter 'sigma' (scale parameter)

pd.sigma

ans = 1

Set parameter 'sigma'

pd.sigma = 2

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 1

sigma = 2

theta = 1

Use this to initialize or modify the scale parameter in a Generalized Pareto distribution. The scale parameter must be a positive real scalar.

Example: 2

Create a Generalized Pareto distribution object by calling its constructor

pd = GeneralizedParetoDistribution (0.5, 2, 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 2

theta = 0

Query parameter 'sigma'

pd.sigma

ans = 2

This shows how to set the scale parameter directly via the constructor, ideal for modeling the spread in extreme value data.

A scalar value characterizing the location of the Generalized Pareto

distribution. You can access the theta property using dot name

assignment.

Example: 1

Create a Generalized Pareto distribution with default parameters

pd = makedist ("GeneralizedPareto")

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 1

sigma = 1

theta = 1

Query parameter 'theta' (location parameter)

pd.theta

ans = 1

Set parameter 'theta'

pd.theta = 1

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 1

sigma = 1

theta = 1

Use this to initialize or modify the location parameter in a Generalized Pareto distribution. The location parameter can be any real scalar, often set to a threshold in extreme value analysis.

Example: 2

Create a Generalized Pareto distribution object by calling its constructor

pd = GeneralizedParetoDistribution (0.5, 1, 1)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 1

Query parameter 'theta'

pd.theta

ans = 1

This demonstrates setting the location parameter directly, useful for shifting the distribution in threshold-exceedance models.

A character vector specifying the name of the probability distribution object. This property is read-only.

A scalar integer value specifying the number of parameters characterizing the probability distribution. This property is read-only.

A cell array of character vectors with each element containing the name of a distribution parameter. This property is read-only.

A cell array of character vectors with each element containing a short description of a distribution parameter. This property is read-only.

A numeric vector containing the values of the distribution

parameters. This property is read-only. You can change the distribution

parameters by assigning new values to the k, sigma, and

theta properties.

A numeric matrix containing the variance-covariance of the parameter estimates. Diagonal elements contain the variance of each estimated parameter, and non-diagonal elements contain the covariance between the parameter estimates. The covariance matrix is only meaningful when the distribution was fitted to data. If the distribution object was created with fixed parameters, or a parameter of a fitted distribution is modified, then all elements of the variance-covariance are zero. This property is read-only.

A logical vector specifying which parameters are fixed and

which are estimated. true values correspond to fixed parameters,

false values correspond to parameter estimates. This property is

read-only.

A numeric vector specifying the truncation interval for the

probability distribution. First element contains the lower boundary,

second element contains the upper boundary. This property is read-only.

You can only truncate a probability distribution with the

truncate method.

A logical scalar value specifying whether a probability distribution is truncated or not. This property is read-only.

A scalar structure containing the following fields:

-

data: a numeric vector containing the data used for distribution fitting. -

cens: a numeric vector of logical values indicating censoring information corresponding to the elements of the data used for distribution fitting. If no censoring vector was used for distribution fitting, then this field defaults to an empty array. -

freq: a numeric vector of non-negative integer values containing the frequency information corresponding to the elements of the data used for distribution fitting. If no frequency vector was used for distribution fitting, then this field defaults to an empty array.

The GeneralizedParetoDistribution class offers the following public methods:

GeneralizedParetoDistribution: p = cdf (pd, x)

GeneralizedParetoDistribution: p = cdf (pd, x,

'upper')

p = cdf (pd, x) computes the CDF of the

probability distribution object, pd, evaluated at the values in

x.

p = cdf (…, returns the complement of

the CDF of the probability distribution object, pd, evaluated at

the values in x.

'upper')

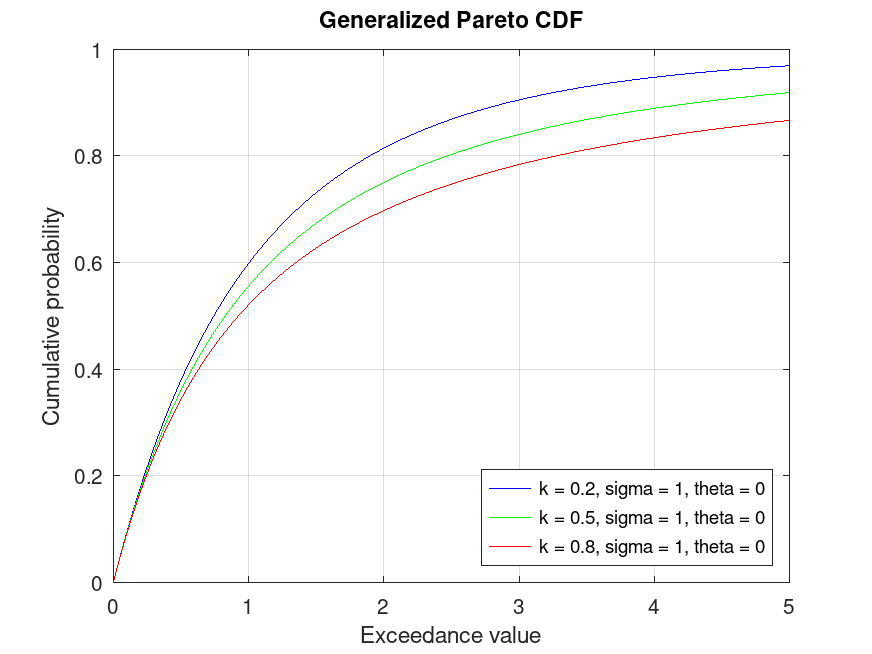

Example: 1

Plot various CDFs from the Generalized Pareto distribution

x = 0:0.01:5;

pd1 = makedist ("GeneralizedPareto", "k", 0.2, "sigma", 1, "theta", 0);

pd2 = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0);

pd3 = makedist ("GeneralizedPareto", "k", 0.8, "sigma", 1, "theta", 0);

p1 = cdf (pd1, x);

p2 = cdf (pd2, x);

p3 = cdf (pd3, x);

plot (x, p1, "-b", x, p2, "-g", x, p3, "-r")

grid on

legend ({"k = 0.2, sigma = 1, theta = 0", "k = 0.5, sigma = 1, theta = 0", "k = 0.8, sigma = 1, theta = 0"}, ...

"location", "southeast")

title ("Generalized Pareto CDF")

xlabel ("Exceedance value")

ylabel ("Cumulative probability")

Use this to compute and visualize the cumulative distribution function for different Generalized Pareto distributions, showing how probability accumulates over exceedance values in extreme value modeling.

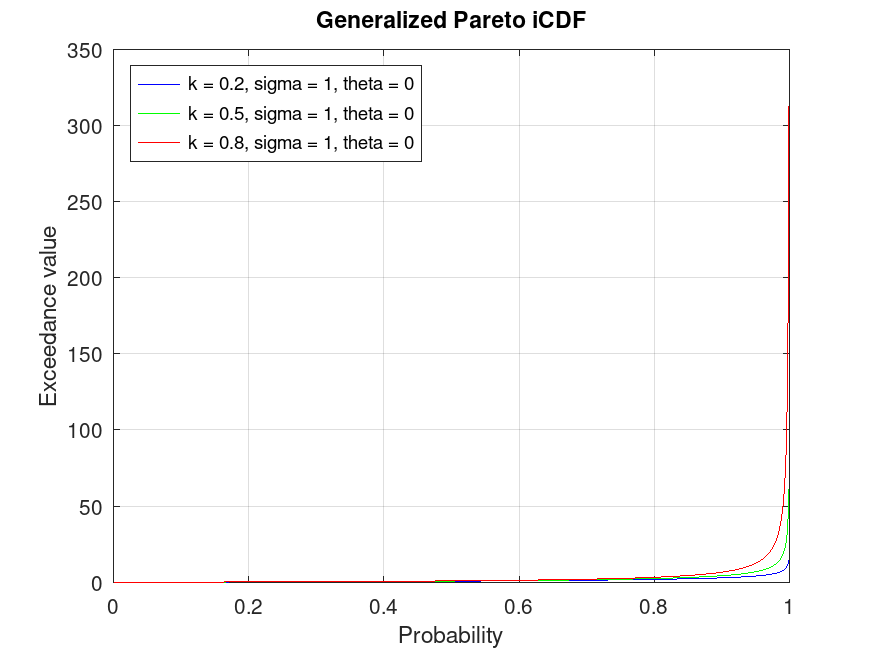

GeneralizedParetoDistribution: x = icdf (pd, p)

x = icdf (pd, p) computes the quantile (the

inverse of the CDF) of the probability distribution object, pd,

evaluated at the values in p.

Example: 1

Plot various iCDFs from the Generalized Pareto distribution

p = 0.001:0.001:0.999;

pd1 = makedist ("GeneralizedPareto", "k", 0.2, "sigma", 1, "theta", 0);

pd2 = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0);

pd3 = makedist ("GeneralizedPareto", "k", 0.8, "sigma", 1, "theta", 0);

x1 = icdf (pd1, p);

x2 = icdf (pd2, p);

x3 = icdf (pd3, p);

plot (p, x1, "-b", p, x2, "-g", p, x3, "-r")

grid on

legend ({"k = 0.2, sigma = 1, theta = 0", "k = 0.5, sigma = 1, theta = 0", "k = 0.8, sigma = 1, theta = 0"}, ...

"location", "northwest")

title ("Generalized Pareto iCDF")

xlabel ("Probability")

ylabel ("Exceedance value")

This demonstrates the inverse CDF (quantiles) for Generalized Pareto distributions, useful for finding the exceedance value corresponding to given return probabilities in risk assessment.

GeneralizedParetoDistribution: r = iqr (pd)

r = iqr (pd) computes the interquartile range of the

probability distribution object, pd.

Example: 1

Compute the interquartile range for a Generalized Pareto distribution

pd = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

iqr_value = iqr (pd)

iqr_value = 1.6906

Use this to calculate the interquartile range, which measures the spread of the middle 50% of the distribution, useful for understanding variability in exceedance values.

GeneralizedParetoDistribution: m = mean (pd)

m = mean (pd) computes the mean of the probability

distribution object, pd.

Example: 1

Compute the mean for different Generalized Pareto distributions

pd1 = makedist ("GeneralizedPareto", "k", 0.2, "sigma", 1, "theta", 0);

pd2 = makedist ("GeneralizedPareto", "k", 0.4, "sigma", 1, "theta", 0);

mean1 = mean (pd1)

mean1 = 1.2500

mean2 = mean (pd2)

mean2 = 1.6667

This shows how to compute the expected exceedance value for Generalized Pareto distributions with different shape parameters (note: mean is finite only if k<1).

GeneralizedParetoDistribution: m = median (pd)

m = median (pd) computes the median of the probability

distribution object, pd.

Example: 1

Compute the median for different Generalized Pareto distributions

pd1 = makedist ("GeneralizedPareto", "k", 0.2, "sigma", 1, "theta", 0);

pd2 = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0);

median1 = median (pd1)

median1 = 0.7435

median2 = median (pd2)

median2 = 0.8284

Use this to find the median exceedance value, which splits the distribution into two equal probability halves.

GeneralizedParetoDistribution: nlogL = negloglik (pd)

nlogL = negloglik (pd) computes the negative

loglikelihood of the probability distribution object, pd.

Example: 1

Compute the negative loglikelihood for a fitted Generalized Pareto distribution

pd = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

rand ("seed", 21);

data = random (pd, 100, 1);

pd_fitted = GeneralizedParetoDistribution.fit (data, 0)

pd_fitted =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.605009 [0.327245, 0.882774]

sigma = 0.958583 [0.697048, 1.31825]

theta = 0

nlogL = negloglik (pd_fitted)

nlogL = -156.27

This is useful for assessing the fit of a Generalized Pareto distribution to data, lower values indicate a better fit.

GeneralizedParetoDistribution: ci = paramci (pd)

GeneralizedParetoDistribution: ci = paramci (pd, Name, Value)

ci = paramci (pd) computes the lower and upper

boundaries of the 95% confidence interval for each parameter of the

probability distribution object, pd.

ci = paramci (pd, Name, Value) computes

the

confidence intervals with additional options specified by

Name-Value pair arguments listed below.

| Name | Value | |

|---|---|---|

'Alpha' | A scalar value in the range specifying the significance level for the confidence interval. The default value 0.05 corresponds to a 95% confidence interval. | |

'Parameter' | A character vector or a cell array of

character vectors specifying the parameter names for which to compute

confidence intervals. By default, paramci computes confidence

intervals for all distribution parameters. |

paramci is meaningful only when pd is fitted to data,

otherwise an empty array, [], is returned.

Example: 1

Compute confidence intervals for parameters of a fitted Generalized Pareto distribution

pd = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

rand ("seed", 21);

data = random (pd, 1000, 1);

[phat, ci] = gpfit (data, 0, 0.05, []);

disp ("Estimated parameters (k, sigma, theta):"), disp (phat)

Estimated parameters (k, sigma, theta): 0.5061 0.9545 0

disp ("95% Confidence Intervals for k and sigma:"), disp (ci)

95% Confidence Intervals for k and sigma: 0.4156 0.8592 0 0.5967 1.0603 0

Use this to obtain confidence intervals for the estimated parameters (k and sigma), providing a range of plausible values given the data (theta is fixed).

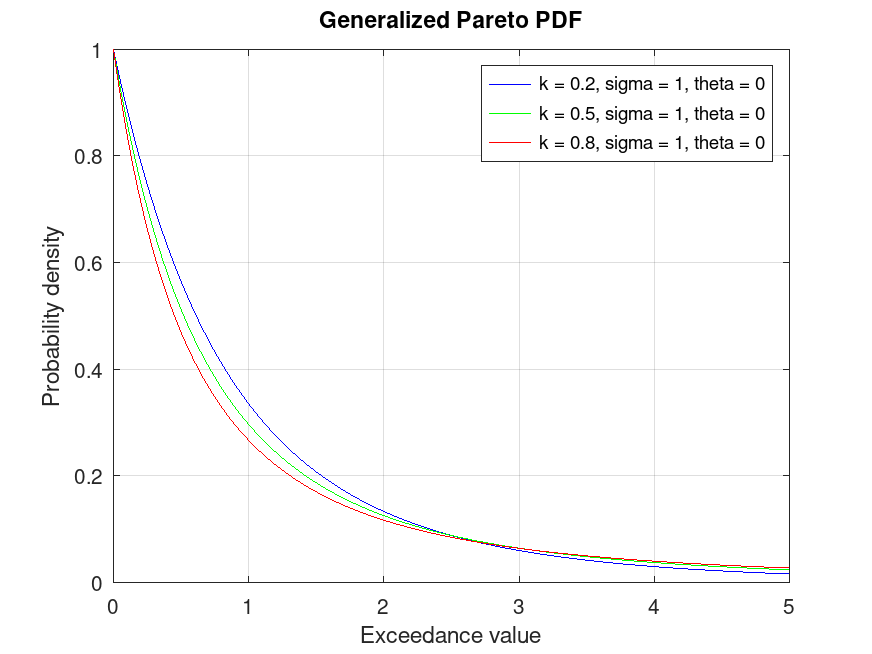

GeneralizedParetoDistribution: y = pdf (pd, x)

y = pdf (pd, x) computes the PDF of the

probability distribution object, pd, evaluated at the values in

x.

Example: 1

Plot various PDFs from the Generalized Pareto distribution

x = 0:0.01:5;

pd1 = makedist ("GeneralizedPareto", "k", 0.2, "sigma", 1, "theta", 0);

pd2 = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0);

pd3 = makedist ("GeneralizedPareto", "k", 0.8, "sigma", 1, "theta", 0);

y1 = pdf (pd1, x);

y2 = pdf (pd2, x);

y3 = pdf (pd3, x);

plot (x, y1, "-b", x, y2, "-g", x, y3, "-r")

grid on

legend ({"k = 0.2, sigma = 1, theta = 0", "k = 0.5, sigma = 1, theta = 0", "k = 0.8, sigma = 1, theta = 0"}, ...

"location", "northeast")

title ("Generalized Pareto PDF")

xlabel ("Exceedance value")

ylabel ("Probability density")

This visualizes the probability density function for Generalized Pareto distributions, showing the likelihood of different exceedance values.

GeneralizedParetoDistribution: plot (pd)

GeneralizedParetoDistribution: plot (pd, Name, Value)

GeneralizedParetoDistribution: h = plot (…)

plot (pd) plots a probability density function (PDF) of the

probability distribution object pd. If pd contains data,

which have been fitted by fitdist, the PDF is superimposed over a

histogram of the data.

plot (pd, Name, Value) specifies additional

options with the Name-Value pair arguments listed below.

| Name | Value | |

|---|---|---|

'PlotType' | A character vector specifying the plot

type. 'pdf' plots the probability density function (PDF). When

pd is fit to data, the PDF is superimposed on a histogram of the

data. 'cdf' plots the cumulative density function (CDF). When

pd is fit to data, the CDF is superimposed over an empirical CDF.

'probability' plots a probability plot using a CDF of the data

and a CDF of the fitted probability distribution. This option is

available only when pd is fitted to data. | |

'Discrete' | A logical scalar to specify whether to

plot the PDF or CDF of a discrete distribution object as a line plot or a

stem plot, by specifying false or true, respectively. By

default, it is true for discrete distributions and false

for continuous distributions. When pd is a continuous distribution

object, option is ignored. | |

'Parent' | An axes graphics object for plot. If

not specified, the plot function plots into the current axes or

creates a new axes object if one does not exist. |

h = plot (…) returns a graphics handle to the plotted

objects.

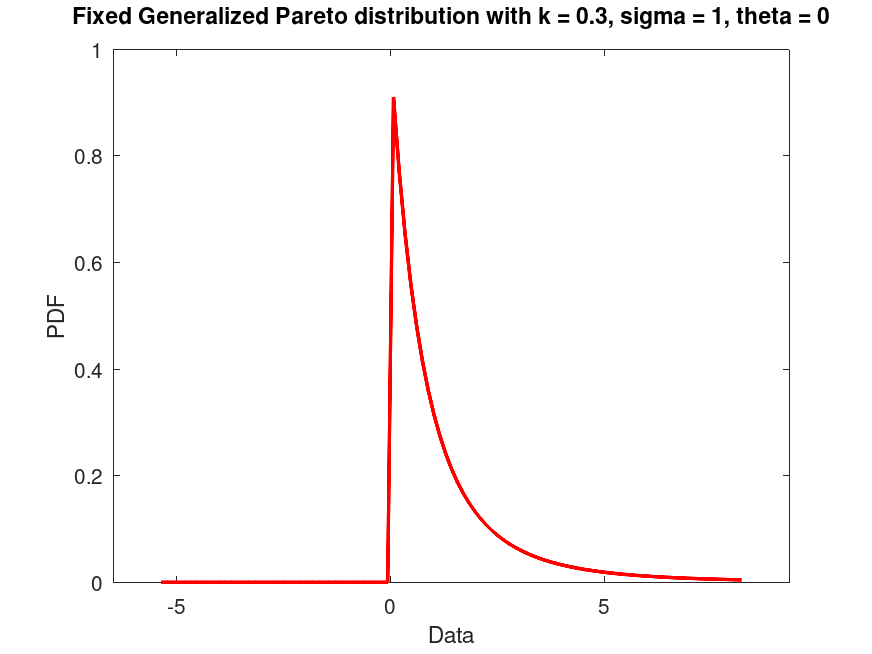

Example: 1

Create a Generalized Pareto distribution with fixed parameters k = 0.5, sigma = 1, theta = 0 and plot its PDF.

pd = makedist ("GeneralizedPareto", "k", 0.3, "sigma", 1, "theta", 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.3

sigma = 1

theta = 0

plot (pd)

title ("Fixed Generalized Pareto distribution with k = 0.3, sigma = 1, theta = 0")

Example: 2

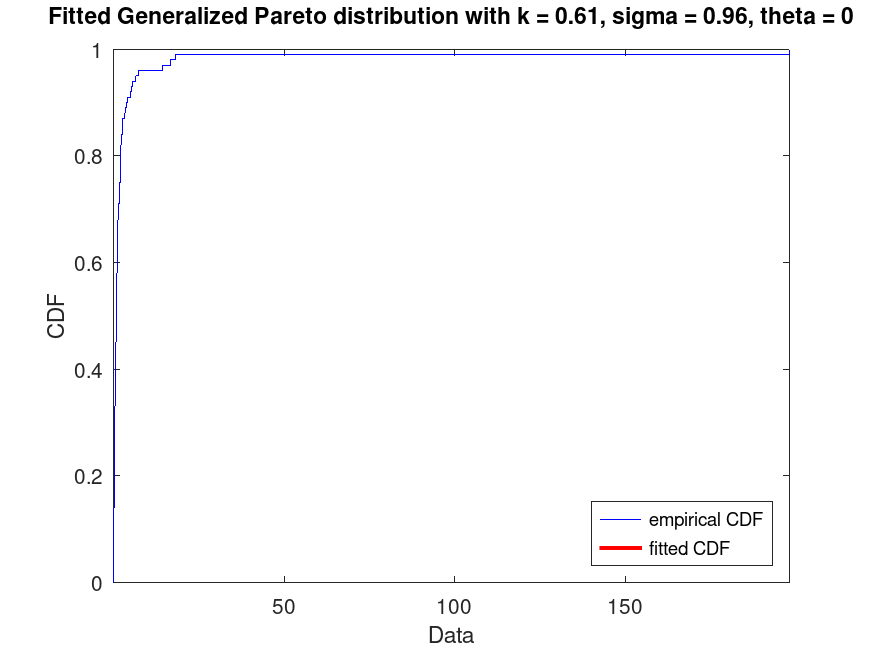

Generate a data set of 100 random samples from a Generalized Pareto distribution with parameters k = 0.5, sigma = 1, theta = 0. Fit a Generalized Pareto distribution to this data (fixing theta=0) and plot its CDF superimposed over an empirical CDF.

pd_fixed = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0)

pd_fixed =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

rand ("seed", 21);

data = random (pd_fixed, 100, 1);

pd_fitted = GeneralizedParetoDistribution.fit (data, 0)

pd_fitted =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.605009 [0.327245, 0.882774]

sigma = 0.958583 [0.697048, 1.31825]

theta = 0

plot (pd_fitted, "PlotType", "cdf")

txt = "Fitted Generalized Pareto distribution with k = %0.2f, sigma = %0.2f, theta = 0";

title (sprintf (txt, pd_fitted.k, pd_fitted.sigma))

legend ({"empirical CDF", "fitted CDF"}, "location", "southeast")

Use this to visualize the fitted CDF compared to the empirical CDF of the data, useful for assessing model fit in extreme value analysis.

Example: 3

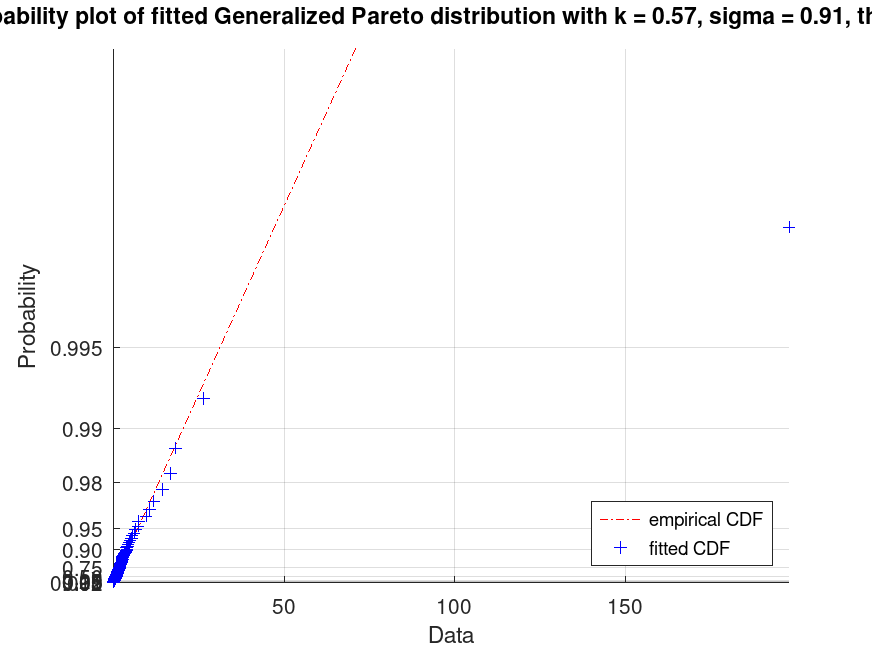

Generate a data set of 200 random samples from a Generalized Pareto distribution with parameters k = 0.5, sigma = 1, theta = 0. Display a probability plot for the Generalized Pareto distribution fit to the data (fixing theta=0).

pd_fixed = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0)

pd_fixed =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

rand ("seed", 21);

data = random (pd_fixed, 200, 1);

pd_fitted = GeneralizedParetoDistribution.fit (data, 0)

pd_fitted =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.571492 [0.367911, 0.775073]

sigma = 0.907212 [0.718512, 1.14547]

theta = 0

plot (pd_fitted, "PlotType", "probability")

txt = strcat ("Probability plot of fitted Generalized Pareto", ...

" distribution with k = %0.2f, sigma = %0.2f, theta = 0");

title (sprintf (txt, pd_fitted.k, pd_fitted.sigma))

legend ({"empirical CDF", "fitted CDF"}, "location", "southeast")

This creates a probability plot to compare the fitted distribution to the data, useful for checking if the Generalized Pareto model is appropriate for tails.

GeneralizedParetoDistribution: [nlogL, param] = proflik (pd, pnum)

GeneralizedParetoDistribution: [nlogL, param] = proflik (pd, pnum,

'Display', display)GeneralizedParetoDistribution: [nlogL, param] = proflik (pd, pnum, setparam)

GeneralizedParetoDistribution: [nlogL, param] = proflik (pd, pnum, setparam,

'Display', display)

[nlogL, param] = proflik (pd, pnum)

returns a vector nlogL of negative loglikelihood values and a

vector param of corresponding parameter values for the parameter in

the position indicated by pnum. By default, proflik uses

the lower and upper bounds of the 95% confidence interval and computes

100 equispaced values for the selected parameter. pd must be

fitted to data.

[nlogL, param] = proflik (pd, pnum,

also plots the profile likelihood

against the default range of the selected parameter.

'Display', 'on')

[nlogL, param] = proflik (pd, pnum,

setparam) defines a user-defined range of the selected parameter.

[nlogL, param] = proflik (pd, pnum,

setparam, also plots the profile

likelihood against the user-defined range of the selected parameter.

'Display', 'on')

For the Generalized Pareto distribution, pnum = 1 selects

the parameter k, pnum = 2 selects the parameter

sigma, and pnum = 3 selects the parameter

theta.

When opted to display the profile likelihood plot, proflik also

plots the baseline loglikelihood computed at the lower bound of the 95%

confidence interval and estimated maximum likelihood. The latter might

not be observable if it is outside of the used-defined range of parameter

values.

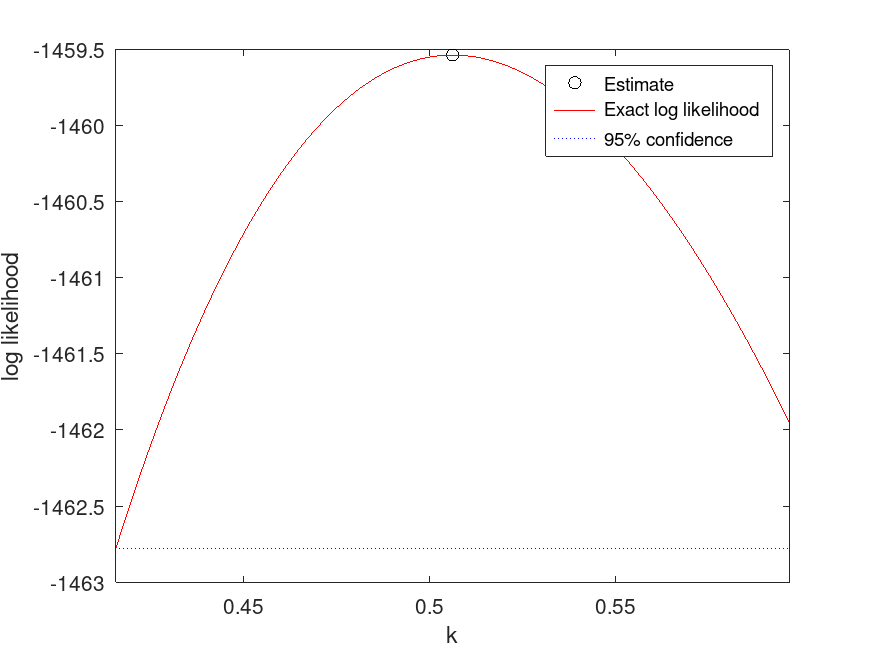

Example: 1

Compute and plot the profile likelihood for the shape parameter of a fitted Generalized Pareto distribution

pd = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

rand ("seed", 21);

data = random (pd, 1000, 1);

pd_fitted = GeneralizedParetoDistribution.fit (data, 0)

pd_fitted =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.506107 [0.415558, 0.596656]

sigma = 0.9545 [0.85923, 1.06033]

theta = 0

[nlogL, param] = proflik (pd_fitted, 1, "Display", "on");

Use this to analyze the profile likelihood of the shape parameter (k), helping to understand the uncertainty in parameter estimates for tail behavior.

GeneralizedParetoDistribution: r = random (pd)

GeneralizedParetoDistribution: r = random (pd, rows)

GeneralizedParetoDistribution: r = random (pd, rows, cols, …)

GeneralizedParetoDistribution: r = random (pd, [sz])

r = random (pd) returns a random number from the

distribution object pd.

When called with a single size argument, random returns a square

matrix with the dimension specified. When called with more than one

scalar argument, the first two arguments are taken as the number of rows

and columns and any further arguments specify additional matrix

dimensions. The size may also be specified with a row vector of

dimensions, sz.

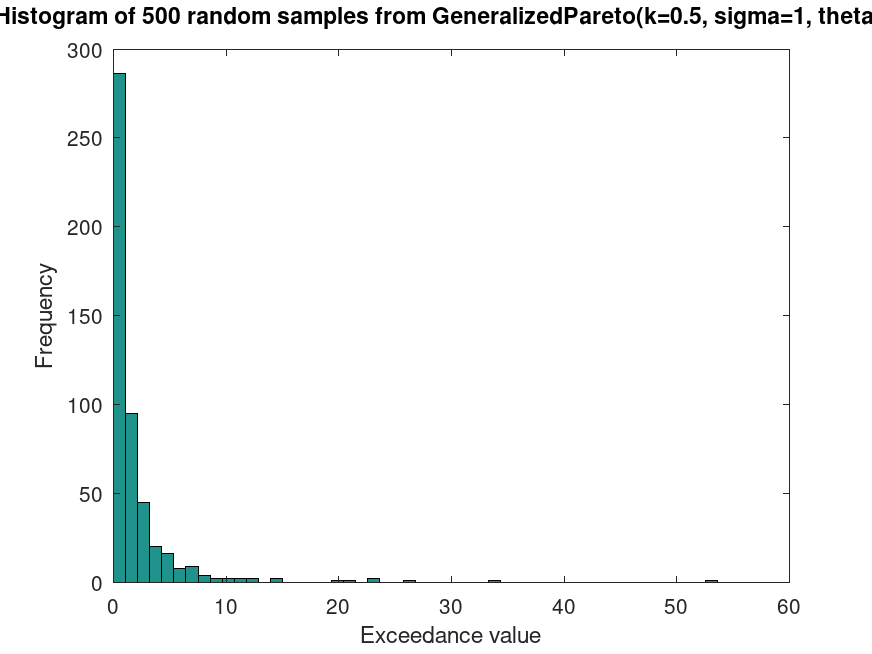

Example: 1

Generate random samples from a Generalized Pareto distribution

pd = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

rand ("seed", 25);

samples = random (pd, 500, 1);

hist (samples, 50)

title ("Histogram of 500 random samples from GeneralizedPareto(k=0.5, sigma=1, theta=0)")

xlabel ("Exceedance value")

ylabel ("Frequency")

This generates random samples from a Generalized Pareto distribution, useful for simulating extreme exceedances in risk modeling.

GeneralizedParetoDistribution: s = std (pd)

s = std (pd) computes the standard deviation of the

probability distribution object, pd.

Example: 1

Compute the standard deviation for a Generalized Pareto distribution

pd = makedist ("GeneralizedPareto", "k", 0.3, "sigma", 1, "theta", 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.3

sigma = 1

theta = 0

std_value = std (pd)

std_value = 2.2588

Use this to calculate the standard deviation, which measures the variability in exceedance values (finite only if k<0.5).

GeneralizedParetoDistribution: t = truncate (pd, lower, upper)

t = truncate (pd, lower, upper) returns a

probability distribution t, which is the probability distribution

pd truncated to the specified interval with lower limit,

lower,

and upper limit, upper. If pd is fitted to data with

fitdist, the returned probability distribution t is not

fitted, does not contain any data or estimated values, and it is as it

has been created with the makedist function, but it includes the

truncation interval.

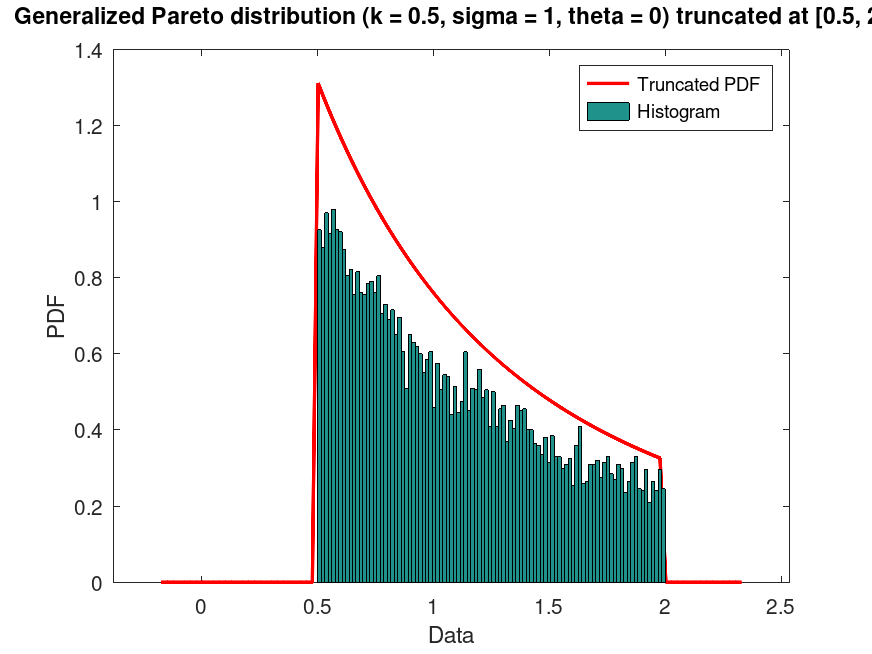

Example: 1

Plot the PDF of a Generalized Pareto distribution, with parameters k = 0.5, sigma = 1, theta = 0, truncated at [0.5, 2] intervals. Generate 10000 random samples from this truncated distribution and superimpose a histogram scaled accordingly

pd = makedist ("GeneralizedPareto", "k", 0.5, "sigma", 1, "theta", 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

t = truncate (pd, 0.5, 2)

t =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.5

sigma = 1

theta = 0

Truncated to the interval [0.5, 2]

rand ("seed", 21);

data = random (t, 10000, 1);

Plot histogram and fitted PDF

plot (t)

hold on

hist (data, 100, 50)

hold off

title ("Generalized Pareto distribution (k = 0.5, sigma = 1, theta = 0) truncated at [0.5, 2]")

legend ("Truncated PDF", "Histogram")

This demonstrates truncating a Generalized Pareto distribution to a specific range and visualizing the resulting distribution with random samples.

GeneralizedParetoDistribution: v = var (pd)

v = var (pd) computes the variance of the

probability distribution object, pd.

Example: 1

Compute the variance for a Generalized Pareto distribution

pd = makedist ("GeneralizedPareto", "k", 0.3, "sigma", 1, "theta", 0)

pd =

GeneralizedParetoDistribution

Generalized Pareto distribution

k = 0.3

sigma = 1

theta = 0

var_value = var (pd)

var_value = 5.1020

Use this to calculate the variance, which quantifies the spread of the exceedance values in the distribution (finite only if k<0.5).